7.5% Salaried professional discount

10% Young family discount (all are 40 years or below at first inception, and will continue for the lifetime of the policy, irrespective of claims.

No Entry Age Limit

Supercharge bonus; optional cover: Get bonus of 100% of sum insured every year, irrespective of claims; max up to 500% of base sum insured.

No CO- PAY with Room rent limit of Single Private a/c Room.

No Zone CO-Pay for Medicare Premier, Select, Top Up Plan

optional cover Must Have – Consumables Coverage, Preventive Health Checkup, Supercharge bonus

BP, Sugar – No loading for Fresh Business.

Policy Wordings

TATA AIG General Insurance Company Limited (We, Our or Us) will provide the insurance, described in this Policy and any endorsements thereto, for the Policy Period, as defined in the Policy to the Insured Person(s) named in the Policy Schedule based on the Disclosure to Information Norm, including in reliance upon the statements contained in the Proposal Form or any other mode of communication which shall be the basis of this Policy and are deemed to be incorporated herein in return for the receipt of the required premium in full and compliance with all the applicable terms, conditions and exclusions of this Policy. The insurance provided under this Policy is only in force for the Insured Person with respect to such and so many of the benefits as indicated in the Policy Schedule and up to the Sum Insured/limits set opposite such benefit(s).

The statements contained in the Proposal signed by the Policyholder (You) shall be the basis of this Policy and are deemed to be incorporated herein. The insurance cover is governed by and subject to, the terms, conditions and exclusions of this Policy.

Your Obligations

Please disclose all pre-existing disease/s or condition/s before buying a policy. Non-disclosure may result in claim not being paid and termination of Your policy.

ABCD, Surgeries, Treatment,

Regular Medication: Now a days single Tablets for combination of Diseases are prescribed, so if you hide some issues, it will be known at the time of Hospitalization, and claim will be rejected.

Preamble

While the policy is in force, if the Insured Person contracts any disease or suffers from any illness or sustains bodily injury through accident and if such event requires the insured Person to incur expenses for Medically Necessary Treatment, We will indemnify You for the amount of such Reasonable and Customary Charges or compensate to the extent agreed, upto the limits mentioned, subject to terms and conditions of the Policy. Each Benefit is subject to its Sum Insured, but Our liability in aggregate to make payment in respect of any and all Benefits shall be limited to the Sum Insured unless expressly stated to the contrary.

In case of family floater policy, the sum insured for all or any of the benefits shall be on a per policy per year basis unless explicitly stated to the contrary. In case of individual policy, the sum insured for all or any of the benefits shall be on per insured per year basis unless explicitly stated to the contrary.

The said Medically Necessary Treatment must be on the advice of a qualified Medical Practitioner.

PRODUCT HIGHLIGHTS

- Professional Discount FOR SALARIED CUSTOMERS, No Entry Age Limit -7.5%

- Young Family Discount FOR FAMILIES BELOW 40 YEARS – 10%

Suitability

| Entry Age: Minimum | Child– 0 days Dependent children between 0 days and 5 years can be insured only when both parents are getting insured. Adult– 18 years |

| Entry Age: Maximum | Child– 25 years Adult– No limit (Life Long eg: 100) |

| Cover Ceasing age | There is no maximum cover ceasing age under this policy. |

| Policy Term | 1 Year/ 2 Years/ 3 Years |

| Renewal | Life long renewal |

| Coverage Options | Individual/Family floater / Multi Individual (1 – 10) |

| Age of Proposer | 18 years or above |

| Relationships Covered | The family includes spouse, economically dependent children and parents/parents-in-law. Relationships covered: Self, spouse and up to 3 dependent children, up to 2 parents and up to 2 parent-in-laws. In case of family floater, where the dependent child(ren) attains 26 years of age at renewal, the child(ren) can be covered under a separate policy with eligible continuity benefit. The Multi-individual policy covers Self, Spouse/ Partners, Upto 3 Dependent Children, Parents & Parents-in-law, Grandparents, Grandchildren, Siblings (Sister/Brother), Uncle, Aunt, Nephew, Niece, Employee, Domestic Help and Legal Guardian. i.e SELF SPOUSE SON DAUGHTER FATHER MOTHER FATHER IN LAW MOTHER IN LAW SISTER BROTHER SISTER IN LAW BROTHER IN LAW GRAND SON GRAND DAUGHTER GRAND FATHER GRAND MOTHER |

| Discount | Long term Discount: 5% for a policy term of 2 years 7.5% for a policy term of 3 years Note: better go with Long Term of 3 years, so that your premium will be Locked, as based on the Claims, Every Insurance company will request IRDAI to increase their Premium in order to settle the claim and for their Survival, so, every company will increase premium up to 12% on Renewals, Instead of 5 years Slab. Professional Discount: 7.5% of discount (This discount is applicable for salaried customers), (PF No. is mandatory to avail this discount.) Young Family Discount: 10% of discount is applicable only if all the Insured Persons covered are of age of 40 years or below at the time of first inception of the policy. This discount will be effective from the first year of the policy and will continue for the lifetime of the policy, irrespective of claims. This discount will be discontinued if, at any point during the policy year, a new member is added whose entry age in policy is 40 years or above. Favorable Experience Discount: 20% at the inception of the policy. At Renewal, the Favorable Experience Discount may vary based on established criteria. Note: First Time Purchase is Zero Year and Renewal years will be First, Second and Third etc… |

| Claim Years in last 3 Policy Years | Favorable Experience Discount |

| 3 Years | 0% |

| 2 Years | 5% |

| 1 Year | 10% |

| No Claim | 20% |

Sum Insured options (in ₹) :

- 5 Lacs

- 7.5 Lacs

- 10 Lacs

- 15 Lacs

- 20 Lacs

- 25 Lacs

- 50 Lacs

- 75 Lacs

- 100 Lacs

- 200 Lacs

- 300 Lacs (3CR)

Zone(s)

For the purpose of premium computation, the country is divided into following three Zones and premium payable under this Policy will be computed based on the zone as applicable for the ‘Address’ of the proposer/ Insured Person:

| Zone A | Mumbai (including Mumbai Metropolitan Region), Delhi (including National Capital Region, Faridabad, Ghaziabad), Ahmedabad, Surat, Baroda and Hisar |

| Zone B | Hyderabad (including Secunderabad), Sangareddy, Bengaluru, Kolkata (including Kolkata Metropolitan Area, Howrah, Hoogly), Indore, Gwalior, Chennai, Chandigarh (including, Mohali, Punchkula, Zirakpur), Pune (including Pimpri Chinchwad), Rajkot, Gandhinagar, Patan, Mahesana, Sabarkantha, Banaskantha, Junagadh, Navsari, Kheda, Arvalli, Mahisagar, and Surendranagar |

| Zone C | Rest of India |

Here ‘Address’ implies the place where the person ordinarily resides. In case proposed prospect(s) reside at multiple addresses, then address of the person residing in the highest zone will be considered.

Lifelong renewal:

We offer you a lifelong renewal for your policy provided premium is paid without any break. Your premiums will be basis the age, sum insured, zone, optional cover(s) and applicable discounts, if any. Your renewal premium will be basis your age on renewal and applicable discounts, if any. There will be no extra loadings based on your individual claim.

The policy is renewable except in the case of established fraud or non-disclosure or misrepresentation by the Insured Person.

Pre-policy medical check-up:

Pre-Policy Check-up at our network may be required based upon the age and/or Sum Insured. The medical reports are valid for a period of 90 days from the date of Pre-Policy Checkup.

| Age(Yrs)/Sum Insured | Up to 50 Lacs | 75 Lacs & 100 Lacs | 200 Lacs & 300 Lacs |

| Upto age 45 | Tele/Video MER (only if positive medical declaration) | Tele/Video MER | |

| 46 – 55 | Tele/Video MER | ||

| 56 – 65 | Tele/Video MER | Tele MER, Subsequently targeted PPC. List of Tests – MER, Urine Routine, CBC with ESR, LFT, RFT, Lipid Profile, Hba1c, ECG | *MER, Urine Routine, CBC with ESR, LFT, RFT, Lipid Profile, Hba1c, ECG |

| 65-75 | *MER, Urine Routine, CBC with ESR, LFT, RFT, Lipid Profile, Hba1c, ECG |

| Above 75 | *MER, CBC ESR, HbA1c, Lipid Profile, Sr. Creatinine, SGOT, SGPT, Urine Routine, 2 D Echo, USG |

- *MER – Medical Examination Report,

- CBC – Complete Blood Count,

- ESR – Erythrocyte Sedimentation Rate ,

- LFT – Liver Function test,

- RFT – Renal Function Test,

- Hba1c – Hemoglobin A1C Test,

- ECG – Electro Cardiogram,

- PPC – Pre-Policy Check-up ,

- SGOT-Serum glutamic-oxaloacetic transaminase,

- SGPT- Serum glutamic pyruvic transaminase,

- USG- Ultrasound Sonography

– Port Proposals, Specially 56 – 65 age, targeted PPC will be advised after Tele / Video MER.

– In case of adverse medical declaration or portability, we may call for additional medical tests. We may conduct medical tests at diagnostic centre/ through home visit, based on medical disclosure wherever applicable.

– 100% of TeleMER cost would be borne by the Company, in case of proposal acceptance.

– *At least 50% of pre-policy medical checkup cost would be borne by Tata AIG in case where proposal is accepted.

– Financial underwriting may be done in case of higher sum insured options.

– The medical reports are valid for a period of 90 days from the date of Pre-Policy Checkup.

website www.tataaig.com.

Section 1 – Definitions

The terms defined below and at other junctures in the Policy Wording have the meanings ascribed to them wherever they appear in this Policy and where appropriate, references to the singular include references to the plural; references to the male includes other genders and references to any statutory enactment includes subsequent changes to the same.

i. Standard Definitions

1. Accident

An Accident means sudden, unforeseen and involuntary event caused by external, visible and violent means.

2. Any one Illness

Any one Illness means continuous period of Illness and includes relapse within 45 days from the date of last consultation with the Hospital/Nursing Home where treatment was taken.

3. AYUSH Day Care Centre

AYUSH Day Care Centre means and includes Community Health Centre (CHC), Primary Health Centre (PHC), Dispensary, Clinic, Polyclinic or any such health centre which is registered with the local authorities, wherever applicable and having facilities for carrying out treatment procedures and medical or surgical/para-surgical interventions or both under the supervision of registered AYUSH Medical Practitioner (s) on day care basis without in-patient services and must comply with all the following criterion:

i. Having qualified registered AYUSH Medical Practitioner(s) in charge;

ii. Having dedicated AYUSH therapy sections as required and/or has equipped operation theatre where Surgical Procedures are to be carried out;

iii. Maintaining daily records of the patients and making them accessible to the insurance company’s authorized representative.

4. AYUSH Hospital

An AYUSH Hospital is a healthcare facility wherein medical/surgical/para-surgical treatment procedures and interventions are carried out by AYUSH Medical Practitioner(s) comprising of any of the following:

a. Central or State Government AYUSH Hospital or

b. Teaching Hospital attached to AYUSH college recognized by the Central Government/ Central Council of Indian Medicine/ Central Council for Homeopathy, or

c. AYUSH Hospital, standalone or co-located with in-patient healthcare facility of any recognized system of medicine, registered with the local authorities, wherever applicable, and is under the supervision of a qualified registered AYUSH Medical Practitioner and must comply with all the following criterion:

i. Having atleast 5 in-patient beds;

ii. Having qualified AYUSH Medical Practitioner in charge round the clock;

iii. Having dedicated AYUSH therapy sections as required and/or has equipped operation theatre where Surgical Procedures are to be carried out;

iv. Maintaining daily records of the patients and making them accessible to the insurance company’s authorized representative.

5. AYUSH Treatment

AYUSH Treatment refers to the medical and / or Hospitalization treatments given under Ayurveda, Yoga and Naturopathy, Unani, Siddha and Homeopathy systems.

6. Break in Policy

Break in Policy means the period of gap that occurs at the end of the existing Policy term/installment premium due date, when the premium due for Renewal on a given Policy or installment premium due is not paid on or before the premium Renewal date or Grace Period.

7. Cashless facility

Cashless facility means a facility extended by the Insurer to the insured where the payments, of the costs of treatment undergone by the insured in accordance with the Policy terms and conditions, are directly made to the Network Provider by the Insurer to the extent pre-authorization is approved.

8. Condition Precedent

Condition Precedent means a Policy terms or condition upon which the Insurer’s liability under the Policy is conditional upon.

9. Congenital Anomaly

Congenital Anomaly means a condition which is present since birth, and which is abnormal with reference to form, structure or position.

a. Internal Congenital Anomaly

Congenital Anomaly which is not in the visible and accessible parts of the body.

b. External Congenital Anomaly

Congenital Anomaly which is in the visible and accessible parts of the body.

10. Cumulative Bonus

Cumulative Bonus means any increase or addition in the Sum Insured granted by the Insurer without an associated increase in premium.

11. Day Care Centre

A Day Care Centre means any institution established for Day Care Treatment of Illness and/or injuries or a medical setup with a Hospital and which has been registered with the local authorities, wherever applicable, and is under supervision of a registered and qualified Medical Practitioner AND must comply with all minimum criterion as under –

i. has qualified nursing staff under its employment;

ii. has qualified Medical Practitioner/s in charge;

iii. has fully equipped operation theatre of its own where Surgical Procedures are carried out;

iv. maintains daily records of patients and will make these accessible to the insurance company’s authorized personnel.

12. Day Care Treatment

Day Care Treatment means medical treatment, and/or Surgical Procedure which is:

i. undertaken under General or Local Anesthesia in a Hospital/Day Care Centre in less than 24 hrs because of technological advancement, and

ii. which would have otherwise required Hospitalization of more than 24 hours. Treatment normally taken on an out-patient basis is not included in the scope of this definition.

13. Dental Treatment

Dental Treatment means a treatment related to teeth or structures supporting teeth including examinations, fillings (where appropriate), crowns, extractions and Surgery.

14. Domiciliary hospitalization

Domiciliary hospitalization means medical treatment for an Illness/disease/Injury which in the normal course would require care and treatment at a Hospital but is actually taken while confined at home under any of the following circumstances:

i. the condition of the patient is such that he/she is not in a condition to be removed to a Hospital, or

ii. the patient takes treatment at home on account of non-availability of room in a Hospital.

15. Emergency Care

Emergency Care means management for an Illness or Injury which results in symptoms which occur suddenly and unexpectedly, and requires immediate care by a Medical Practitioner to prevent death or serious long term impairment of the Insured Person’s health.

16. Grace Period

“Grace Period” means the specified period of time, immediately following the premium due date during which premium payment can be made to renew or continue a Policy in force without loss of continuity benefits pertaining to waiting periods and coverage of Pre-Existing Diseases.

For single premium payment policies, coverage is not available during the period for which no premium is received. However, If the premium is paid in instalments during the Policy Period, coverage will be available during the Grace Period, within the Policy Period.

The Grace Period for payment of the premium shall be: fifteen days where premium payment mode is monthly and thirty days in all other cases.

17. Hospital

A Hospital means any institution established for Inpatient Care and Day Care Treatment of Illness and/or injuries and which has been registered as a Hospital with the local authorities under Clinical Establishments (Registration and Regulation) Act 2010 or under enactments specified under the Schedule of Section 56(1) of the said act Or complies with all minimum criteria as under:

i. has qualified nursing staff under its employment round the clock;

ii. has at least 10 in-patient beds in towns having a population of less than 10,00,000 and at least 15 in-patient beds in all other places;

iii. has qualified Medical Practitioner(s) in charge round the clock;

iv. has a fully equipped operation theatre of its own where Surgical Procedures are carried out;

v. maintains daily records of patients and makes these accessible to the insurance company’s authorized personnel;

18. Hospitalization

Hospitalization means admission in a Hospital for a minimum period of 24 consecutive ‘Inpatient Care’ hours except for specified procedures/ treatments, where such admission could be for a period of less than 24 consecutive hours.

19. Illness

Illness means a sickness or a disease or pathological condition leading to the impairment of normal physiological function and requires medical treatment.

a. Acute condition

Acute condition is a disease, Illness or Injury that is likely to respond quickly to treatment which aims to return the person to his or her state of health immediately before suffering the disease/ Illness/ Injury which leads to full recovery

b. Chronic condition

A chronic condition is defined as a disease, Illness, or Injury that has one or more of the following characteristics:

i. it needs ongoing or long-term monitoring through consultations, examinations, check-ups, and /or tests

ii. it needs ongoing or long-term control or relief of symptoms

iii. it requires rehabilitation for the patient or for the patient to be specially trained to cope with it

iv. it continues indefinitely

v. it recurs or is likely to recur

20. Injury

Injury means accidental physical bodily harm excluding Illness or disease solely and directly caused by external, violent, visible and evident means which is verified and certified by a Medical Practitioner.

21. Inpatient Care

Inpatient Care means treatment for which the Insured Person has to stay in a Hospital for more than 24 hours for a covered event.

22. Intensive Care Unit:

Intensive Care Unit means an identified section, ward or wing of a Hospital which is under the constant supervision of a dedicated Medical Practitioner(s), and which is specially equipped for the continuous monitoring and treatment of patients who are in a critical condition, or require life support facilities and where the level of care and supervision is considerably more sophisticated and intensive than in the ordinary and other wards.

23. ICU Charges:

ICU (Intensive Care Unit) Charges means the amount charged by a Hospital towards ICU expenses which shall include the expenses for ICU bed, general medical support services provided to any ICU patient including monitoring devices, critical care nursing and intensivist charges.

General Note: An intensivist is a board-certified physician who provides special care for critically ill patients.

24. Maternity Expenses:

Maternity Expenses means;

a. medical treatment expenses traceable to childbirth (including complicated deliveries and caesarean sections incurred during Hospitalization);

b. expenses towards lawful medical termination of pregnancy during the Policy Period.

25. Medical Advice

Medical Advice means any consultation or advice from a Medical Practitioner including the issuance of any prescription or follow-up prescription.

26. Medical Expenses:

Medical Expenses means those expenses that an Insured Person has necessarily and actually incurred for medical treatment on account of Illness or Accident on the advice of a Medical Practitioner, as long as these are no more than would have been payable if the Insured Person had not been insured and no more than other Hospitals or doctors in the same locality would have charged for the same medical treatment.

27. Medical Practitioner

Medical Practitioner means a person who holds a valid registration from the Medical Council of any State or Medical Council of India or Council for Indian Medicine or for Homeopathy set up by the Government of India or a State Government and is thereby entitled to practice medicine within its jurisdiction; and is acting within its scope and jurisdiction of license.

28. Medically Necessary Treatment

Medically Necessary Treatment means any treatment, tests, medication, or stay in Hospital or part of a stay in Hospital which:

i. is required for the medical management of the Illness or Injury suffered by the insured;

ii. must not exceed the level of care necessary to provide safe, adequate and appropriate medical care in scope, duration, or intensity;

iii. must have been prescribed by a Medical Practitioner;

iv. must conform to the professional standards widely accepted in international medical practice or by the medical community in India.

29. Migration

“Migration” means a facility provided to policyholders (including all members under family cover and group policies), to transfer the credits gained for Pre-Existing Diseases and specific waiting periods from one health insurance Policy to another with the same Insurer.

30. Network Provider

Network Provider means Hospitals or health care providers enlisted by an Insurer, TPA or jointly by an Insurer and TPA to provide medical services to an insured by a Cashless facility.

The updated list of Network Provider is available on Our website (www.tataaig.com).

31. New Born Baby

New Born Baby means baby born during the Policy Period and is aged upto 90 days.

32. Non-Network Provider

Non-Network means any Hospital, Day Care Centre or other provider that is not part of the network.

33. Notification of Claim

Notification of Claim means the process of intimating a claim to the Insurer or TPA through any of the recognized modes of communication.

34. OPD treatment

OPD treatment means the one in which the Insured visits a clinic / Hospital or associated facility like a consultation room for diagnosis and treatment based on the advice of a Medical Practitioner. The Insured is not admitted as a day care or in-patient.

35. Pre-Existing Disease

“Pre-Existing Disease (PED)” means any condition, ailment, Injury or disease:

a. that is/are diagnosed by a physician not more than 36 months prior to the date of commencement of the Policy issued by the Insurer; or

b. for which Medical Advice or treatment was recommended by, or received from, a physician, not more than 36 months prior to the date of commencement of the Policy.

36. Pre-hospitalization Medical Expenses

Pre-hospitalization Medical Expenses means Medical Expenses incurred during predefined number of days preceding the Hospitalization of the Insured Person, provided that:

i. Such Medical Expenses are incurred for the same condition for which the Insured Person’s Hospitalization was required, and

ii. The In-patient Hospitalization claim for such Hospitalization is admissible by the Insurance Company.

37. Portability

“Portability” means a facility provided to the health insurance policyholders (including all members under family cover), to transfer the credits gained for, Pre-Existing Diseases and specific waiting periods from one Insurer to another Insurer.

38. Post-hospitalization Medical Expenses

Post-hospitalization Medical Expenses means Medical Expenses incurred during predefined number of days immediately after the Insured Person is discharged from the Hospital provided that:

i. Such Medical Expenses are for the same condition for which the Insured Person’s Hospitalization was required, and

ii. The inpatient Hospitalization claim for such Hospitalization is admissible by the insurance company.

39. Qualified Nurse

Qualified Nurse means a person who holds a valid registration from the Nursing Council of India or the Nursing Council of any state in India.

40. Reasonable and Customary charges

Reasonable and Customary charges means the charges for services or supplies, which are the standard charges for the specific provider and consistent with the prevailing charges in the geographical area for identical or similar services, taking into account the nature of the Illness / Injury involved.

General Note: to avoid unnecessary stress better go to network hospitals)

41. Renewal

Renewal means the terms on which the contract of insurance can be renewed on mutual consent with a provision of Grace Period for treating the Renewal continuous for the purpose of gaining credit for Pre-Existing Diseases, time-bound exclusions and for all waiting periods.

42. Room Rent

Room Rent means the amount charged by a Hospital towards Room and Boarding expenses and shall include the Associated Medical Expenses.

43. Surgery or Surgical Procedure

Surgery or Surgical Procedure means manual and / or operative procedure (s) required for treatment of an Illness or Injury, correction of deformities and defects, diagnosis and cure of diseases, relief from suffering and prolongation of life, performed in a Hospital or Day Care Centre by a Medical Practitioner.

44. Unproven/Experimental treatment

Unproven/Experimental treatment means the treatment including drug experimental therapy which is not based on established medical practice in India, is treatment experimental or unproven.

ii. Specific Definitions (Definitions other than as mentioned under Section 1 (i) above)

1. Age

Means the completed Age of the Insured Person on his / her last birthday as on date of commencement of the Policy and as per the English calendar.

2. Aggregate Deductible

Aggregate Deductible is a cost sharing requirement under this Policy which provides that We will not be liable for a specified amount in aggregate for all claims during the per Policy Year. A deductible does not reduce the Sum Insured.

3. Associated Medical Expenses (AME)

AME shall include nursing charges, operation theatre charges, fees of Medical Practitioner/surgeon/ anesthetist/ specialist (excluding cost of pharmacy and consumables, cost of implants and medical devices, cost of diagnostics) conducted within the same Hospital where the Insured Person has been admitted. It shall not be applicable for Hospitalization in ICU. Associated Medical Expenses shall be applicable for covered expenses, incurred in Hospitals which follow differential billing based on the room category.

4. Multi-Sharing Accommodation

Multi-Sharing Accommodation means a Hospital room with three or more patient beds. This definition does not apply to ICU or ICCU.

5. Modern Treatment Methods and Advancement in Technologies

The following Procedures shall be considered for Modern Treatment Methods and Advancement in Technologies: (12)

A. Uterine Artery Embolization and HIFU

B. Balloon Sinuplasty

C. Deep Brain stimulation

D. Oral chemotherapy

E. Immunotherapy-Monoclonal Antibody to be given as injection

F. Intra vitreal injections

G. Robotic surgeries

H. Stereotactic radiosurgeries

I. Bronchical Thermoplasty

J. Vaporisation of the prostrate (Green laser treatment or holmium laser treatment)

K. IONM – (Intra Operative Neuro Monitoring)

L. Stem cell therapy: Hematopoietic stem cells for bone marrow transplant for haematological conditions to be covered.

6. Policy

Policy means the contract of insurance including but not limited to Policy Schedule, Endorsements,

Policy Wordings (inbuilt covers & optional covers, if opted), Riders, Annexures etc., as applicable.

7. Policy Period

Policy Period means the time during which this Policy is in effect. Such period commences from Commencement Date and ends on the Expiry Date and specifically appears in the Policy Schedule.

8. Policy Schedule

Policy Schedule means the Policy Schedule attached to and forming part of Policy.

9. Policy Year

Policy Year means a period of twelve consecutive months beginning from the date of commencement of the Policy Period and ending on the last day of such twelve-month period.

For the purpose of subsequent years, Policy Year shall mean a period of twelve months commencing from the end of the previous Policy Year and lapsing on the last day of such twelve-month period, or the Policy Expiry date whichever is earlier.

10. Single Private Room

Single Private Room means an air-conditioned room in a Hospital where a single patient is accommodated and which has an attached toilet (lavatory and bath). Such room type shall be the most basic and the most economical of all accommodations available as a single occupancy room in that Hospital.

This does not include a deluxe room or a suite or a VIP room. Any room that offers services or incurs charges greater than those of the Single Private Room shall be classified as a room category higher than the Single Private Room.

11. Sum Insured

“Sum Insured” refers to the amount specified in the Policy Schedule at the inception of a Policy Year, excluding any Bonus. Sum Insured represents Our maximum, total and cumulative liability under the Policy, for all the Insured Person(s) covered in aggregate, for the respective Policy Year.

• Upon the successful admission of a claim, the Sum Insured for the remaining Policy Year shall be accordingly reduced by the amount of the claim settled (inclusive of ‘taxes’) or admitted.

• In cases where the Policy Period is 2/3 years, the specified Sum Insured in the Policy Schedule signifies the limit for the initial Policy Year. This limit shall expire at the conclusion of the first year, and fresh limit up to the opted Sum Insured will become available for the subsequent second/third year, unless specified otherwise

12. Twin Sharing Accommodation

Twin Sharing Accommodation means a Hospital room with two patient beds. This definition does not apply to ICU or ICCU. Such room type shall be the most basic and the most economical of all accommodations available as twin sharing room in that Hospital.

13. We, Us, Our, Insurer

means The TATA AIG General Insurance Company Limited that has provided Insurance Cover under this Policy.

14. You, Your, Insured Person

means the person whose name specifically appears in the Policy Schedule as an Insured Person/ Policyholder.

15. Zone(s)

For the purpose of premium computation, the country is divided into following three Zones and premium payable under this Policy will be computed based on the Zone as applicable for the ‘Address’ of the proposer/ Insured Person:

• Zone A: Mumbai (including Mumbai Metropolitan Region), Delhi (including National Capital Region, Faridabad, Ghaziabad), Ahmedabad, Surat, Baroda and Hisar

• Zone B: Hyderabad (including Secunderabad), Sangareddy, Bengaluru, Kolkata (including Kolkata Metropolitan Area, Howrah, Hoogly), Indore, Gwalior, Chennai, Chandigarh (including, Mohali, Punchkula, Zirakpur), Pune (including Pimpri Chinchwad), Rajkot, Gandhinagar, Patan, Mahesana, Sabarkantha, Banaskantha, Junagadh, Navsari, Kheda, Arvalli, Mahisagar, and Surendranagar

• Zone C: Rest of India

Here ‘Address’ implies the place where the person ordinarily resides. In case proposed prospect(s) reside at multiple addresses, then address of the person residing in the highest Zone will be considered.

Please note that the above-mentioned categorization of zones is subject to change at Our sole discretion. Any such change made which shall impact an existing policyholder, shall be intimated under 3 months’ notice and shall be applicable from the immediate next Renewal.

Section 2 – Benefits

If during the Policy Period one or more Insured Person(s) is required to be hospitalized for treatment (including Modern Treatment Methods and Advancement in Technologies) of an Illness or Injury at a Hospital / Day Care Centre, following Medical Advice of a duly qualified Medical Practitioner, the Company shall indemnify Medically Necessary expenses towards the coverage mentioned in the Policy Schedule for the amount of such Reasonable and Customary charges or compensate to the extent agreed, upto the limits mentioned, subject to terms and conditions of the Policy . Provided further that, any amount payable under the Policy shall be subject to the terms of coverage (including Aggregate Deductible, if opted), exclusions, conditions and definition contained herein. Maximum liability of the Company under all such Claims during each Policy Year shall be the Sum Insured opted and Cumulative Bonus (if accrued), as specified in the Policy Schedule (except in case of a claim under Infinite Advantage (if opted) or Early Access (if opted)).

In case of family floater Policy, the Sum Insured, Cumulative Bonus & Aggregate Deductible, if applicable, shall be available for all Insured Persons on an aggregate basis, on a per Policy Year basis.

B1. In-Patient Treatment

We will cover Medical Expenses for Medically Necessary Treatment in a Hospital due to disease/Illness/Injury (covered event), for period more than 24 hrs., that requires an Insured Person’s admission in a Hospital for an Inpatient Care, during the Policy Period.

Medical Expenses directly related to the Hospitalization would be payable.

The Company shall indemnify Medical Expenses as listed below:

i. Room Rent, Boarding, Nursing Expenses as provided by the Hospital / Nursing Home, up to the room category specified in the Policy Schedule.

ii. Intensive Care Unit (ICU) / Intensive Cardiac Care Unit (ICCU) expenses

iii. Surgeon, Anesthetist, Medical Practitioner, Consultants, Specialist Fees

iv. Anesthesia, Qualified Nurse charges, blood, oxygen, operation theatre charges, surgical appliances, medicines, drugs, costs towards diagnostics, diagnostic imaging modalities and such similar other expenses.

If the Insured Person is admitted in a room whose category is higher than the one that is specified in the Policy Schedule, then the Insured Person shall bear a rateable proportion of the Room Rent and the total Associated Medical Expenses, including surcharge or taxes thereon in the proportion of the ‘difference between the Room Rent actually incurred & the Room Rent of the entitled room category’ to ‘the Room Rent actually incurred’.

• Proportionate deductions are not applicable for ICU Charges.

• Such proportionate deductions, if any, will not be applied in respect of the Hospitals which do not follow differential billing or for those Associated Medical Expenses in respect of which differential billing is not adopted based on the room category.

Benefit Specific Sub-limit: Room Category –Upto Single private room. For category applicable to you, please refer your Policy Schedule.

Limit for In-Patient Treatment- Upto Sum Insured

B2. Pre-Hospitalization expenses

We will cover expenses for pre-hospitalization consultations, investigations and medicines incurred upto 90 days prior to the date of admission to the Hospital. Any pre-hospitalization expenses incurred prior to Policy Period shall not be covered.

The benefit is payable if We have admitted a claim under B1, B4, or B6.

Limit for Pre-Hospitalization expenses- Upto 90 days, Upto Sum Insured

B3. Post-Hospitalization expenses

We will cover expenses for post-hospitalization consultations, investigations and medicines incurred upto 90 days after discharge from the Hospital.

The benefit is payable if We have admitted a claim under B1, B4, or B6.

Limit for Post-Hospitalization expenses- Upto 90 days, Upto Sum Insured

B4. Day Care Procedures

We will cover expenses for Day Care Treatment, due to disease/Illness/Injury (covered event), taken in a Hospital or a Day Care Centre, during the Policy Period.

Limit for Day Care Procedures- Upto Sum Insured

B5. Organ Donor

We will cover the Medical Expenses, incurred by or in respect of the organ donor, for an organ transplant Surgery, solely towards the harvesting of the organ donated subject to the following conditions:

i. The organ donation conforms to the Transplantation of Human Organs (Amendment) Bill, 2011 and the organ is for the use of the Insured Person;

ii. The Insured Person is the recipient of the organ so donated by the organ donor and the claim of such Surgery is accepted by Us under B1 of this Policy;

iii. The organ transplant is medically necessary for the Insured Person as certified by a Medical Practitioner

iv. Claim under this section shall be assessed as per the claim of the recipient Insured Person

What is not covered (Addl. Information compared to premier)

i. Pre-hospitalization Medical Expenses or Post hospitalization Medical Expenses of the organ donor

ii. Screening Expenses of the organ donor

iii. Any other medical expense as a result of harvesting from the organ donor

iv. Costs directly or indirectly associated with the acquisition of the donor’s organ.

v. Transplant of any organ/tissue where the transplant is experimental or investigational

vi. Expenses related to organ transportation or preservation

vii. Any other medical treatment or complication in respect of the donor, consequent to harvesting.

Limit for Organ Donor- Upto Sum Insured

B6. Domiciliary Treatment

We will cover expenses related to Domiciliary hospitalization of the Insured Person if the treatment exceeds beyond three consecutive days and is availed during the Policy Period. The treatment must be for management of an Illness and not for enteral feedings or end of life care.

At the time of claiming under this benefit, We shall require certification from the treating doctor fulfilling the conditions as mentioned under the general definitions (Section 1) of this Policy.

Limit for Domiciliary Treatment- Upto Sum Insured

B7. AYUSH Benefit

We will cover Medical Expenses incurred for treatment as In-Patient or Day Care in an AYUSH Hospital/ AYUSH Day Care Centre, for a room category, as specified in the Policy Schedule and applicability of Associated Medical Expenses.

This benefit shall also cover Pre-hospitalization Medical Expenses for a period of upto 90 days before the date of admission to the AYUSH Hospital/ AYUSH Day Care Centre and Post-hospitalization Medical Expenses for a period upto 90 days, subject to AYUSH In-Patient Hospitalization or AYUSH Day Care Treatment claim being admissible under this benefit.

Claims under this section shall be assessed as per the applicable insurance guidelines related to AYUSH and benchmark rates as available on Ministry of AYUSH website (https://ayushnext.ayush.gov.in/site/insurance-guidelines-related-to-ayush).

For reference, please refer the document “Annexure B for AYUSH Benefit” available on Our website (www.tataaig.com)

Limit for AYUSH Benefit- Upto Sum Insured

B8. Ambulance Cover (Road)

We will cover expenses incurred for the transportation of the Insured Person in a registered road ambulance, within a radius of 50 kilometers, (Addl. Information compared to premier) for the following:

i. In case of an emergency, from site of incident to the nearest Hospital for admission

ii. If medically necessary and prescribed by the treating practitioner, from Insured Person’s residence to Hospital

iii. From one Hospital to another Hospital for better medical facilities and treatment or from one Hospital to diagnostic center for advanced diagnostic treatment, where such facility is not available at the existing Hospital.

iv. If medically necessary and prescribed by the treating practitioner, from Hospital to Insured Person’s residence

For this claim to be paid, the claim must be admissible under B1 or B4 of this Policy.

Limit for Ambulance Cover- Upto Sum Insured

B9. Restore Infinity Plus (- for both Related + Unrelated)

We will provide reinstatement of the base Sum Insured, if the Sum Insured and Cumulative Bonus (if accrued) is insufficient to pay an admissible Hospitalization claim in the Policy. The reinstatement will be available for unlimited number of times during a Policy Year, subject to below conditions:

i. This benefit shall not be available for the first admissible Hospitalization/ Domiciliary Treatment claim in each Policy Year. The Sum Insured will be restored for the subsequent claim in the Policy Year.

ii. In case of Family Floater Policy, reinstatement of Sum Insured will be available for all Insured Persons in the Policy on floater basis.

iii. The unutilized restored Sum Insured cannot be carried forward to the next Policy Year.

iv. This benefit shall also be applicable annually for policies with tenure of more than 1 year.

v. Any restored Sum Insured can only be utilized for an admissible claim under following indemnity covers of the Policy, as applicable:

a. In-Patient Treatment,

b. Pre/Post Hospitalization expenses,

c. Day Care Procedures,

d. Organ donor,

e. Domiciliary Treatment,

f. AYUSH Benefit,

g. Ambulance Cover,

h. Consumable benefit (If opted)

vi. Any restored Sum Insured under this benefit cannot be utilized for an admissible claim under:

a. Any cover other than the ones mentioned in the above section or

b. Any cover which has Sum Insured over and above the base Sum Insured.

vii. Our maximum liability in aggregate of all claims arising out of a single Hospitalization shall not exceed the Sum Insured of the base Policy.

Note: No 45 Days waiting period or Restriction on Dialysis or Cancer Treatment.

B10. Daily Cash for choosing Twin Sharing Accommodation

We will pay a fixed amount per day as mentioned in the Policy Schedule, if the Insured Person is Hospitalized in a Twin Sharing Accommodation (2 Patients), for each continuous and completed period of 24 hours.

Payout under this benefit is only available if the room category eligibility applicable under this Policy is ‘Single Private Room’ or room category higher than the Single Private Room.

This benefit has a separate limit (over and above base Sum Insured) and does not affect No Claim Bonus.

Optional Sub-limit: Twin Sharing accommodation — Room Category Select

Limit for Daily Cash for choosing Twin Sharing Accommodation- Rs.1200 per day (over and above base sum insured)

B11. Daily Cash for choosing Multi-Sharing Accommodation

We will pay a fixed amount per day as mentioned in the Policy Schedule, if the Insured Person is Hospitalized in a Multi-Sharing Accommodation (More Than 2 Patients) , for each continuous and completed period of 24 hours.

Payout under this benefit is only available if the room category eligibility applicable under this Policy is ‘Single Private Room’ or room category higher than the Single Private Room.

This benefit has a separate limit (over and above base Sum Insured) and does not affect No Claim Bonus.

Limit for Daily Cash for choosing Multi-Sharing Accommodation- Rs.1500 per day (over and above base sum insured)

Note: Sharing Room Discount is not suggested to Opt, as during Hospitalization, mostly you will go to Single Room only then you have to pay CO-Pay.

B12. No Claim Bonus

Note: if you opt for Super Charge Bonus then this benefit wont be applicable.

Under this section, the below mentioned ‘No claim Bonus’ options will be available and applicable as opted by You.

Cumulative bonus or Discount in Renewal Premium will be available for every claim free policy year.

Either of the two options is to be selected:

1) Cumulative Bonus

i. 50% Cumulative Bonus will be applied on the Sum Insured of the expiring Policy, on each Renewal after every claim free Policy Year, provided that the Policy is renewed with Us and without a break. The maximum Cumulative Bonus shall not exceed 100% of the Sum Insured in any Policy Year.

ii. If a Cumulative Bonus has been applied and a claim is made, then in the subsequent Policy Year We will automatically decrease the Cumulative Bonus by 50% of the Sum Insured in that following Policy Year. There will be no impact on the base Sum Insured, only the accrued Cumulative Bonus will be decreased.

iii. In policies with a tenure of more than one year, the above guidelines of Cumulative Bonus shall be applicable post completion of each Policy Year.

iv. In relation to a Family Floater, the Cumulative Bonus so applied will only be available in respect of those Insured Person(s) who were Insured Person(s) in the claim free Policy Year and continue to be Insured Person(s) in the subsequent Policy Year.

v. For the purpose of computation of Cumulative Bonus, the percentage (%) of Cumulative Bonus will be applied on the base Sum Insured of the expiring Policy only. The Restore Infinity Plus amount will not be taken into consideration for such computation.

vi. Reduction of Sum Insured: In case the Sum Insured under the Policy is reduced at the time of Renewal then the accrued Cumulative Bonus under this benefit shall be reduced in proportion to the reduced Sum Insured.

vii. Cumulative Bonus will lapse if the Policy is not renewed before Policy expiry (including the Grace Period).

2) Discount in Renewal Premium (No Claim Bonus): (Not Suggested)

If you choose Discount in Renewal Premium, We will allow 1% discount on renewal premium for every claim free Policy Year, provided that the Policy is renewed with Us without break.

Tax Benefit:

The premium amount paid under this policy qualifies for deduction under Section 80D of the Income Tax Act.

Optional Covers

The Optional Cover(s) can only be opted along with the base covers under the Policy and cannot be opted in isolation or as a separate product. The Optional cover(s) are provided on payment of additional premium or discounts and subject to the terms and conditions and exclusions as stated in the Policy Terms and Conditions and Exclusions. These Optional Cover(s), if selected, should be opted for all eligible Insured Persons to be covered under the Policy unless stated otherwise and shall be available only if the same are specifically mentioned in the Policy Schedule.

The insurance provided under these Optional cover(s) are only with respect to such and so many of the coverages as are indicated in the Policy Schedule.

C1. Consumables Benefit (Must & Should Opt)

In consideration of additional premium paid and notwithstanding the exclusion mentioned under Section 3.ii (Specific Exclusions).A.(xii), if this optional cover has been opted, We will cover expenses incurred for specified consumables, subject to balance Sum Insured, which are mentioned in Annexure I – List I of optional items (Consumables Benefit) available on Our website (www.tataaig.com) which are consumed during the period of Hospitalization directly related to the Insured Person’s medical or surgical treatment of Illness/disease/Injury.

Conditions applicable for claim to be admissible under this cover:

o Item is a medical consumable and is medically necessary;

o prescribed by the treating Medical Practitioner and

o the Hospitalization claim is admissible under B1 or B4 of this Policy.

The assessment of payout under this Optional Cover shall follow the assessment of claim done under B1 and B4 except for application of Associated Medical Expenses.

Limit for Consumables Benefit- Upto Sum Insured

C2. Maternity Care (for All 3)

In consideration of additional premium paid and if this optional cover has been opted, We will cover Maternity Expenses, delivery complication of a New Born Baby and First Year Vaccinations of the New Born Baby up to the limits specified in the Policy Schedule.

This benefit has a separate limit (over and above base Sum Insured) and does not affect No Claim Bonus.

The cover is available for the selected Insured Person(s) and is subject to a waiting period of 2 years of continuous coverage of the Insured Person(s) under this cover with Us.

i. Maternity Expenses:

Notwithstanding the exclusion mentioned under Section 3.i (Standard Exclusions).B.(xii) Maternity (Code – Excl 18), We will cover Maternity Expenses related to childbirth and lawful medical termination of pregnancy during the Policy Period.

We will not cover ectopic pregnancy under this benefit; however, it shall be covered under section B1.

The following shall be excluded from the scope of this coverage:

• Expenses incurred for pre/post natal care

• Pre/Post Hospitalization Expenses (Section B2 and B3 of this Policy)

Also, no coverage is available for voluntary termination of pregnancy during the Policy Period under this Policy.

ii. Delivery Complications of New Born Baby:

For complications related to delivery, We will cover Medically Necessary Treatment of the New Born Baby incurred during the Hospitalization, if claim related to childbirth is admissible under the ‘Maternity Expenses’ cover (C2. i) of this Policy.

iii. First year Vaccinations:

We will cover vaccination expenses for the child up to their first birthday, if claim related to childbirth is admissible under the ‘Maternity Expenses’ cover (C2. i) of this Policy and subject to continuity of the Policy with Us.

The limit available under this benefit is a lifetime limit for each child.

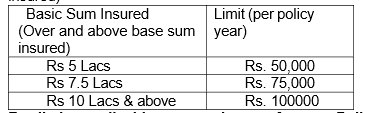

Limit for Maternity Care (all 3 ) – 10% of Sum Insured, maximum up to Rs.1,00,000 per policy year (over and above base sum insured)

C3. Reduction of Maternity Care Waiting Period

In consideration of additional premium paid, the waiting period specified under Section C2 of this Policy shall be reduced to 1 year of continuous coverage.

C4. Infinite Advantage

no limit on the Sum Insured for one claim

In consideration of additional premium paid, We will cover the Medical Expenses incurred for an admissible claim under In-Patient Treatment/Daycare Procedures for any one claim during the lifetime of the Policy, without any limits on the available annual Sum Insured, subject to the following conditions:

i. The cover can be selected only at the inception of the Policy. Once opted, the cover has to be opted continuously under the Policy, until a claim is made under this cover.

ii. All the conditions applicable for the admissibility of In-Patient Treatment/Daycare Procedures cover shall be applicable to this cover

iii. This cover is applicable only for one claim in the lifetime of the Policy.

iv. Once a claim has been made under this Cover, the cover will cease to exist and cannot be opted again upon subsequent Renewals.

v. The available amount shall be utilized as per following sequence in event of a claim under this Optional Cover:

a. Base Sum Insured/ Early Access (if opted)

b. Cumulative Bonus

c. Infinite Advantage (only when the total amount available for claim is exhausted)

vi. After utilization of all the above-mentioned benefits, the total available amount shall be reduced to zero for that Policy Year/tenure (If Early Access has been opted) following the payment of claim under Infinite Advantage.

vii. Room category applicable under this cover shall be as per the room category opted and mentioned in the Policy Schedule

viii. ‘Aggregate Deductible’ or any other cost sharing covers, if opted, shall be applicable under this cover.

C5. Early Access

In consideration of additional premium paid, for single premium multi-year policies, the Sum Insured of the Policy Period shall be available anytime during the Policy Period, for utilization towards an admissible claim under Section B1, B2, B3, B4, B5, B6, B7 or B8.

With Early Access: Your annual Base Sum Insured is combined for the entire tenure opted by You. This combined Base Sum Insured will be available for the entire Policy tenure which means that unutilized Sum Insured, if any, shall be carried forward to the next Policy Year of the same Policy Period.

Illustration

Base Sum Insured (per Policy Year): Rs. 20 Lakhs

Policy Tenure: 3 Years

| Year | Without Early Access | With Early Access |

| Sum Insured (Rs.) | ||

| Year 1 | 20 Lakhs | 60 Lakhs |

| Year 2 | 20 Lakhs | |

| Year 3 | 20 Lakhs | |

| Year 4 | 20 Lakhs | 60 Lakhs |

| Year 5 | 20 Lakhs | |

| Year 6 | 20 Lakhs | |

Explanation:

Without Early Access: If You purchase a Policy of tenure of more than 1 year, Your Policy Sum Insured operates on annual basis. Which means if You have a Policy of Base Sum Insured Rs. 20 Lakhs, You can use Rs. 20 Lakhs in each Policy Year towards admissible claims.

C6. Room Category Select (For HNI)

Any Room (For HNI) Addl premium has to pay or TWIN Sharing Accommodations – Get Discount (not Recommended)

If this optional cover is availed, the room category entitlement in the Policy shall be replaced to the room category as specified in the Policy Schedule.

However, if the Insured Person is admitted in a room whose category is higher than the one that is specified in the Policy Schedule, then the Insured Person shall bear a rateable proportion of the Room.

Rent and the total Associated Medical Expenses, including surcharge or taxes thereon in the proportion of the ‘difference between the Room Rent actually incurred & the Room Rent of the entitled room category’ to ‘the Room Rent actually incurred’.

• Proportionate deductions are not applicable for ICU Charges.

• Such proportionate deductions, if any, will not be applied in respect of the Hospitals which do not follow differential billing or for those Associated Medical Expenses in respect of which differential billing is not adopted based on the room category.

C7. Aggregate Deductible (if you don’t want to claim small amounts)

10K / 25K / 50K / 100K

In consideration of premium discount availed by You, Our liability under this Policy shall be subject to Aggregate Deductible as specified in the Policy Schedule, subject to the following conditions:

i. Aggregate Deductible, shall be applicable on aggregate of final assessed amount of all admissible claims in a Policy Year and Our liability shall be restricted to the balance amount, subject to availability of Sum Insured

ii. In case of multi-year base Policy (i.e. tenure more than 1 year), such Aggregate Deductible would be applicable per Policy Year.

iii. Aggregate Deductible shall be applicable for all indemnity claims under following covers of this Policy, as applicable:

a. In-Patient Treatment,

b. Pre/Post Hospitalization expenses,

c. Day Care Procedures,

d. Organ donor,

e. Domiciliary Treatment,

f. AYUSH Benefit,

g. Ambulance Cover

h. Consumable benefit (if opted)

i. Infinite Advantage (if opted)

j. Early Access (if opted)

C8. Introduction of Valued Provider Network (not Suggested)

Any treatment availed outside Our network of “Valued Provider-Pan India” shall attract a Co-Payment of 30% for each such claim, resulting from admission of the Insured Person in a Hospital/ Day Care Centre/ AYUSH Hospital

Discounts on premium:

| A | Long term discount | 7.5% for a policy term of 3 years 5% for a policy term of 2 years This discount is available only with ‘Single’ Premium Payment mode. | ||||

| B | Family floater discount | 1 member | No Discount | |||

| 2 members | 22% | |||||

| 3 members | Atleast 1 child | 28% | ||||

| No child | 22% | |||||

| 3+ members | Atleast 2 children | 32% | ||||

| Atleast 1 child | 28% | |||||

| No child | 22% | |||||

| C | Multi- Individual Discount | 5% (When more than one member are covered in a policy on individual basis) | ||||

| D | Professional Discount | 7.5% (This discount is applicable for salaried employee of public or a private company) | ||||

| E | Young Family Discount | 10% 1. This discount is applicable only if all the Insured Persons covered are of age of 40 years or below at the time of first inception of the policy. 2. This discount will be effective from the first year of the policy and will continue for the lifetime of the policy, irrespective of claims. 3. This discount will be discontinued if, at any point during the policy year, a new member is added whose entry age in policy is 40 years or above. | ||||

| F | Discount in lieu of commission | Upto 15% |

| G | Favorable Experience Discount | 20% at the inception of the policy. At Renewal, the Favorable Experience Discount may vary based on established criteria. |

Favorable Experience Discount:

At Renewal, the Favorable Experience Discount will depend on below criteria:

| Claim Years in last 3 Policy Years | Discount |

| 3 Years | 0% |

| 2 Years | 5% |

| 1 Year | 10% |

| No Claim | 20% |

Note:

Where ‘Claim Year’ is a Policy year in which one or more claim(s) have been paid. For the purpose of Favorable Experience Discount, a Policy year with claim only under ‘Daily Cash for choosing Twin Sharing Accommodation’, ‘Daily Cash for choosing Multi-Sharing Accommodation’ and ‘Maternity Care’ benefit will not be considered a ‘Claim Year’.

Note: The above mentioned discounts are multiplicative and applied on the base premium. Discounts other than Long term discount, Family floater discount, Multi-Individual Discount, Favorable Experience Discount and Discount in Renewal Premium (No Claim Bonus) are subject to a maximum cap of 25%.

C 9.Supercharge Bonus Rider

We will provide Supercharge Bonus in the form of specified percentage of the base Sum Insured of the expiring Policy, post completion of each Policy Year, irrespective of claims in preceding Policy Years. The total accrued Supercharge Bonus shall not exceed specified percentage of the base Sum Insured in any Policy Year.

Get bonus of 100% of Sum Insured every year, irrespective of claims; Max up to specified percentage of base sum insured.

Inbuilt for Sum insured of Rs.5 Lakhs to Rs. 7.5Lakhs, 100% per policy year, Max up to 300%.

Optional: for Sum Insured of Rs.10Lakhs & above , 100% per policy year, Max up to 300%.

Note: Supercharge Bonus Rider will override the “No claim Bonus” benefit under the product. i.e if you opt this Riders then NCB won’t applicable.

Home Care Treatment Rider

We’ll cover the cost of expenses up to sum insured, incurred for treatment taken at home. The pandemic care will be covered upto 25% of the sum insured.

Accidental Death Benefit Rider

If an Insured Person suffers an accident during the policy period and this is the sole and direct cause of his death within 365 days from the date of accident, then we will pay 100% of the Sum Insured or Rs. 50,00,000, whichever is lower

Advanced Cover Rider (Not Available)

Cut the waiting period for specific pre-existing diseases to just 30 days for faster access to treatment.

Preventive Annual Health Checkup Rider (Not Available)

Get cashless annual health check-ups at home or with our providers, keeping health in check every year, ensuring proactive health management.

OPD Care (Not Available)

Get coverage for OPD Consultation, Dental, Vision and teleconsultations for seamless Outpatient Care.

EmpowerHer (Not Available)

Comprehensive coverage for women’s health, from gynaecologist visits and PCOD treatment to cancer screenings and vaccinations.

Mental Wellbeing (Not Available)

Holistic mental health care with mental health screenings, psychological therapy, stress management, diet consultations, and addiction cessation programs.

Cancer Care:

Suggested only if Family Tree has effected with Cancer.

Section 3 – Exclusions

We will neither be liable nor make any payment for any claim in respect of any Insured Person which is caused by, arising from or in any way attributable to any of the following exclusions. All the waiting periods shall be applicable individually for each Insured Person.

i. Standard Exclusions

A. Exclusions with waiting periods

i. Pre-Existing Diseases Waiting Period (Code- Excl 01):

a. Expenses related to the treatment of a Pre-Existing Disease (PED) and its direct complications shall be excluded until the expiry of 36 months of continuous coverage after the date of inception of the first Policy with Us.

b. In case of enhancement of Sum Insured the exclusion shall apply afresh to the extent of Sum Insured increase.

c. If the Insured Person is continuously covered without any break as defined under the Portability norms of the extant IRDAI (Health Insurance) Regulations, then waiting period for the same would be reduced to the extent of prior coverage.

d. Coverage under the Policy after the expiry of 36 months for any Pre-Existing Disease is subject to the same being declared at the time of application and accepted by Us.

ii. (40 + 1) Specified Disease/Procedure Waiting Period (Code- Excl 02):

(Not applicable for claims arising due to an accident)

a. Expenses related to the treatment of the listed conditions, surgeries/treatments shall be excluded until the expiry of 24 months of continuous coverage after the date of inception of the first Policy with Us. This exclusion shall not be applicable for claims arising due to an Accident.

b. In case of enhancement of Sum Insured, the exclusion shall apply afresh to the extent of Sum Insured increase.

c. If any of the specified disease/procedure falls under the waiting period specified for Pre- Existing Diseases, then the longer of the two waiting periods shall apply.

d. The waiting period for listed conditions shall apply even if contracted after the Policy or declared and accepted without a specific exclusion.

e. If the Insured Person is continuously covered without any break as defined under the applicable norms on Portability stipulated by IRDAI, then waiting period for the same would be reduced to the extent of prior coverage.

List of Specific disease/conditions/treatments:

I. Tumors, Cysts, polyps including breast lumps (benign) (Arbud, Granthi, including arbud in Sthana)

II. Polycystic ovarian disease (garbhashaya granthi),

Fibromyoma {Aartav dushti (Sowmya arbudham)},

Adenomyosis,

Endometriosis (Udavarthani yoni vyaazpt)

III. Prolapsed Uterus (Yoni bhramsha)

IV. Gout and Rheumatism (Vaathraktha and Aamvaat / Aadhya vata), Rheumatoid arthritis, Non-infective arthritis (Sandhi shool {Dhatukshay janya or Avrodhjanya, both, Sandhigata vata, Vata roga})

V. Ligament, Tendon or Meniscal tear (Sira, kandara, maamsgat vaat janya shool, sandhi shola)

VI. Prolapsed Inter-Vertebral Disc (Katishool, Greevashool, Grudhrasi vata) and Spinal Diseases including spondylitis/spondylosis unless arising from Accident

VII. Cholelithiasis (yakrut roga)

VIII. Pancreatitis

IX. Fissure/fistula in anus, haemorrhoids, pilonidal sinus (Arsha, Parikartika, bhagandar, gudagat vranshoth, nadi vrana)

X. Ulcer & erosion of stomach & duodenum

XI. Gastro Esophageal Reflux Disorder (GERD) (Parinamshool, annadravakhya shool, Amlapitta, Grahani)

XII. Liver Cirrhosis

XIII. Perineal Abscesses (bhagandhara)

XIV. Perianal / Anal Abscesses

XV. Calculus diseases of Urogenital system Example: Kidney stone, Urinary bladder stone (Ashmari of all types)

XVI. Benign Hyperplasia of prostate (Asththila vruddhi)

XVII. Varicocele (Vruddhi, Vrushanshoth)

XVIII. Cataract (avrana Shukla),

Retinal detachment,

Glaucoma (abhishyandha)

XIX. Congenital Internal Diseases

XX. Osteoarthritis and osteoporosis (Asthikshay/ asti gata vata)

XXI. Systemic connective tissue disorders, inflammatory polyarthropathies.

List of procedure/surgeries/treatments:

XXII. Adenoidectomy

XXIII. Mastoidectomy

XXIV. Tonsillectomy

XXV. Tympanoplasty

XXVI. Surgery for nasal septum deviation and

Nasal concha resection

XXVII. Surgery for Turbinate hypertrophy

XXVIII. Hysterectomy

XXIX. Joint replacement surgeries (for example: Knee replacement, Hip replacement)

XXX. Cholecystectomy

XXXI. Hernioplasty or Herniorraphy

XXXII. Surgery/procedure for Benign prostate enlargement

XXXIII. Surgery for Hydrocele/ Rectocele/Spermatocele

XXXIV. Surgery of varicose veins and varicose ulcers

XXXV. Obesity / Weight control procedures including Gastric bypass surgeries. (already covered in Code- Excl 06)

iii. 30 Days Waiting Period for all illnesses (Code- Excl 03):

(not applicable for accidents or on renewals)

a. Expenses related to the treatment of any Illness within 30 days from the first Policy commencement date shall be excluded except claims arising due to an Accident, provided the same are covered.

b. This exclusion shall not, however, apply if the Insured Person has Continuous Coverage for more than twelve months.

c. The within referred waiting period is made applicable to the enhanced Sum Insured in the event of granting higher Sum Insured subsequently.

B. Medical Exclusions ( 12 + (10 + 2) = 24)

i. Investigation and evaluation (Code- Excl 04):

a. Expenses related to any admission primarily for diagnostics and evaluation purposes only are excluded.

b. Any diagnostic expenses which are not related or not incidental to the current diagnosis and treatment are excluded.

ii. Rest cure, rehabilitation and respite care (Code- Excl 05):

a. Expenses related to any admission primarily for enforced bed rest and not for receiving treatment. This also includes:

i. Custodial care either at home or in a nursing facility for personal care such as help with activities of daily living such as bathing, dressing, moving around either by skilled nurses or assistant or non-skilled persons.

ii. Any services for people who are terminally ill to address physical, social, emotional and spiritual needs.

iii. Obesity/ Weight Control (Code- Excl 06):

Expenses related to surgical treatment of obesity that does not fulfil the below conditions:

a. Surgery to be conducted is upon the advice of the Doctor.

b. The Surgery/Procedure conducted should be supported by clinical protocols.

c. The member has to be 18 years of Age or older and

d. Body Mass Index (BMI);

i. greater than or equal to 40 or

ii. greater than or equal to 35 in conjunction with any of the following severe co-morbidities following failure of less invasive methods of weight loss:

1. Obesity-related cardiomyopathy

2. Coronary heart disease

3. Severe Sleep Apnea

4. Uncontrolled Type2 Diabetes

iv. Change-of-Gender treatments (Code- Excl07):

Expenses related to any treatment, including surgical management, to change characteristics of the body to those of the opposite sex.

v. Cosmetic or Plastic Surgery (Code- Excl 08):

Expenses for cosmetic or plastic Surgery or any treatment to change appearance unless for reconstruction following an Accident, Burn(s) or Cancer or as part of Medically Necessary Treatment to remove a direct and immediate health risk to the Insured Person. For this to be considered a medical necessity, it must be certified by the attending Medical Practitioner.

vi. Treatment for Alcoholism, drug or substance abuse or any addictive condition and consequences thereof (Code- Excl 12).

vii. Treatments received in health hydros, nature cure clinics, spas or similar establishments or private beds registered as a nursing home attached to such establishments or where admission is arranged wholly or partly for domestic reasons. (Code- Excl13)

viii. Dietary supplements and substances that can be purchased without prescription, including but not limited to Vitamins, minerals and organic substances unless prescribed by a Medical Practitioner as part of Hospitalization claim or day care procedure. (Code-Excl14)

ix. Refractive error (Code- Excl 15):

Expenses related to the treatment for correction of eye sight due to refractive error less than 7.5 dioptres.

x. Unproven treatments (Code- Excl 16):

Expenses related to any Unproven Treatment, services and supplies for or in connection with any treatment. Unproven treatments are treatments, procedures or supplies that lack significant medical documentation to support their effectiveness.

xi. Sterility and Infertility (Code- Excl 17):

Expenses related to Sterility and infertility. This includes:

i. Any type of contraception, sterilization

ii. Assisted Reproduction services including artificial insemination and advanced reproductive technologies such as IVF, ZIFT, GIFT, ICSI

iii. Gestational Surrogacy

iv. Reversal of sterilization

xii. Maternity (Code – Excl 18):

1. Medical treatment expenses traceable to childbirth (including complicated deliveries and caesarean sections incurred during Hospitalization) except ectopic pregnancy;

2. Expenses towards miscarriage (unless due to an Accident) and lawful medical termination of pregnancy during the Policy Period.

C. Non-Medical Exclusions (3 + 14 = 17)

i. Hazardous or Adventure Sports (Code- Excl 09):

Expenses related to any treatment necessitated due to participation as a professional in hazardous or adventure sports, including but not limited to, para-jumping, rock climbing, mountaineering, rafting, motor racing, horse racing or scuba diving, hand gliding, sky diving, deep-sea diving.

ii. Breach of law (Code- Excl 10):

Expenses for treatment directly arising from or consequent upon any Insured Person committing or attempting to commit a breach of law with criminal intent.

iii. Excluded Providers: (Code-Excl 11):

Expenses incurred towards treatment in any Hospital or by any Medical Practitioner or any other provider specifically excluded by the Insurer and disclosed in its website / notified to the Policyholders are not admissible. However, in case of life-threatening situations or following an Accident, expenses up to the stage of stabilization are payable but not the complete claim.

ii. Specific Exclusions (Exclusions other than as those mentioned under Section 3 (i) subsection A, B & C above)

We will neither be liable nor make any payment for any claim in respect of any Insured Person

which is caused by, arising from or in any way attributable to any of the following exclusions.

A. Medical Exclusions

i. Alcoholic pancreatitis or Alcoholic liver disease;

ii. Congenital External Diseases, defects or anomalies;

iii. Stem cell therapy; however, hematopoietic stem cells for bone marrow transplant for haematological conditions will be covered under this Policy,

iv. Growth Hormone Therapy;

v. Sleep-apnoea and Sleeping disorder;

vi. Admission primarily for administration (via any form or mode) of immunoglobulin infusion or supplementary medications like Zolendronic Acid, etc;

vii. Venereal disease, sexually transmitted disease or Illness;

viii. All preventive care including Health Check-ups, vaccination including inoculation and immunisations;

ix. Cost of dentures, dental implants and braces; Dental Treatment or Dental Surgery of any kind unless incidental to an admissible Hospitalization claim where the cause of admission is Accident;

x. Any form of Non-Allopathic treatment (except AYUSH Benefit), Hydrotherapy, Acupuncture, Reflexology, Chiropractic treatment or any other form of indigenous system of medicine.

xi. Any existing disease specifically mentioned as Permanent exclusion in the Policy Schedule.

xii. Non payable items as mentioned in Annexure I – List I of optional items available on Our website (www.tataaig.com) —as it is Add on

B. Non-Medical Exclusions

i. War or any act of war, invasion, act of foreign enemy, war like operations (whether war be declared or not) or caused during service in the armed forces of any country, civil war, public defence, rebellion, revolution, insurrection, military or usurped acts, nuclear weapons/materials, chemical and biological weapons, ionising radiation.

ii. Nuclear, chemical or biological attack or weapons, contributed to, caused by, resulting from or from any other cause or event contributing concurrently or in any other sequence to the loss, claim or expense. For the purpose of this exclusion: (irrelevant)

• Nuclear attack or weapons means the use of any nuclear weapon or device or waste or combustion of nuclear fuel or the emission, discharge, dispersal, release or escape of fissile/ fusion material emitting a level of radioactivity capable of causing any Illness, incapacitating disablement or death

• Chemical attack or weapons means the emission, discharge, dispersal, release or escape of any solid, liquid or gaseous chemical compound which, when suitably distributed, is capable of causing any Illness, incapacitating disablement or death.

• Biological attack or weapons means the emission, discharge, dispersal, release or escape of any pathogenic (disease producing) micro-organisms and/or biologically produced toxins (including genetically modified organisms and chemically synthesized toxins) which are capable of causing any Illness, incapacitating disablement or death.

iii. Any Insured Person’s participation or involvement in naval, military or air force operation.

iv. Intentional self-Injury or attempted suicide while sane or insane.

v. If the Insured Person is under the influence of intoxicating liquor or drugs or other intoxicants, except where the Insured Person is not directly responsible for the Injury/Accident though under influence of intoxication.

vi. Items of personal comfort and convenience like television (wherever specifically charged for), charges for access to telephone and telephone calls, internet, foodstuffs (except patient’s diet), cosmetics, hygiene articles, body care products and bath additive, barber or beauty service, guest service.

vii. Treatment rendered by a Medical Practitioner which is outside his discipline.

viii. Doctor’s fees charged by the Medical Practitioner sharing the same residence as an Insured Person or who is an immediate relative of an Insured Person’s family.

ix. Hearing aids, spectacles or contact lenses, etc. including optometric therapy.

x. Any treatment and associated expenses for alopecia, baldness, wigs or toupees, medical supplies including elastic stockings, diabetic test strips and similar products.

xi. Any treatment or part of a treatment that does not form part of ‘Reasonable and Customary charges’, nor is medically necessary;

xii. Expenses which are either not supported by a prescription of a Medical Practitioner or are not related to Illness or disease for which claim is admissible under the Policy.

xiii. Any external appliance and/or device used for diagnosis or treatment except when used intra-operatively. eg: Crutches

xiv. Any Illness diagnosed or Injury sustained or where there is change in health status of the member after date of proposal and before commencement of Policy and the same is not communicated and accepted by Us.

No Need to Know from here

Section 4 – General Terms and Clauses

i. Standard General Terms & Clauses

1. Disclosure of Information

The Policy shall be void and all premium paid thereon shall be forfeited to the Company in the event of established fraud, misrepresentation, misdescription or non-disclosure of any material fact by the policyholder.

(Explanation: “Material facts” for the purpose of this Policy shall mean all relevant information sought by the company in the proposal form and other connected documents to enable it to take informed decision in the context of underwriting the risk)

2. Condition Precedent to Admission of Liability

The terms and conditions of the Policy must be fulfilled by the Insured Person for the Company to make any payment for claim(s) arising under the Policy.

3. Claim Settlement (provision for Penal Interest)

i. The Company shall settle or reject a claim, as the case may be, within 15 days from the date of receipt of last necessary document.

ii. In the case of delay in the payment of a claim, the Company shall be liable to pay interest to the policyholder from the date of receipt of last necessary document to the date of payment of claim at a rate 2% above the bank rate.

iii. However, where the circumstances of a claim warrant an investigation in the opinion of the Company, it shall initiate and complete such investigation at the earliest, in any case not later than 30 days from the date of receipt of last necessary document. In such cases, the Company shall settle or reject the claim within 45 days from the date of receipt of last necessary document.