introduction:

The government introduced various incentives in the recent times to encourage the adoption of the new regime. These changes show that the government intends to have taxpayer’s transition to the new regime and eventually phase out the old one. Though the new regime is now the default tax regime, the old tax regime will continue to exist.

The old tax structure encourages taxpayers to cultivate a habit of saving, while the new tax structure favours employees with lower earnings and reducing the potential for tax evasion fraud.

1. How to Choose Between Old and New Tax Regimes?

When deciding between the two tax regimes, it is important to take into account the tax exemptions and deductions available under the old tax regime. After deducting all eligible exemptions and deductions, the net taxable income can be determined. By calculating the tax liability based on this net taxable income under the old tax regime, it becomes possible to compare it with the tax liability under the new tax regime.

Choosing the regime with the lower tax liability is the logical approach, and it is essential to inform the employer about this choice so that the appropriate Tax Deducted at Source (TDS) can be deducted from the salary.

If you have a loss from house property, capital gains, or business & profession, you need to consider them as well while making informed decisions on the selection of regime. Along with the current year’s losses, even the previous year’s losses eligible to set off will get lapsed as well. Ineligibility to carry forward such losses may impact your future income determination and taxes thereon.

2. Current Tax Rates under New Tax Regime

A. New Tax Regime

A new tax regime was introduced in Budget 2020 wherein the tax slabs were altered, and taxpayers were offered concessional tax rates. However, those who opt for the new regime cannot claim several exemptions and deductions, such as HRA, LTA, 80C, 80D , and more. Because of this, the new tax regime did not have many takers. The government in the Budget 2023 introduced 5 key changes, which remain the same even for FY 2024-2025 since no changes were made in the Interim Budget 2024, to encourage taxpayers to adopt the new regime. They are:

- Higher Tax Rebate Limit: Full tax rebate on an income up to ₹7 lakhs is allowed. Whereas this threshold is ₹5 lakhs under the old tax regime. This means that taxpayers with an income of up to ₹7 lakhs will not have to pay any tax at all under the new tax regime!

- Streamlined Tax Slabs: The tax exemption limit is up-to ₹3 lakhs, and the new tax slabs are:

| Tax Slab for FY 2024-25 | Tax Rate |

| Upto ₹ 3 lakh | Nil |

| ₹ 3 lakh – ₹ 7 lakh | 5% |

| ₹ 7 lakh – ₹ 10 lakh | 10% |

| ₹ 10 lakh – ₹ 12 lakh | 15% |

| ₹ 12 lakh – ₹ 15 lakh | 20% |

| More than 15 lakh | 30% |

B. Old Tax Regime

The old regime is the tax system that prevailed before the introduction of the new regime. Under this regime, there are over 70 exemptions and deductions available, including HRA and LTA, that can reduce your taxable income and lower tax payments. The most popular and generous deduction is Section 80C, which allows for a reduction of taxable income up to Rs.1.5 lakh. The taxpayers are given a choice between the old and the new tax regime.

The tax rates under both regimes are compared as below:

| Old Tax Regime (FY 2024-25) | New Tax Regime FY 2024-25 | |||

| Income Slabs | Age < 60 years & NRIs | Age of 60 Years to 80 years | Age above 80 Years | |

| Up to ₹2,50,000 | NIL | NIL | NIL | NIL |

| ₹2,50,001 – ₹3,00,000 | 5% | NIL | NIL | NIL |

| ₹3,00,001 – ₹5,00,000 | 5% | 5% | NIL | 5% |

| ₹5,00,001 – ₹6,00,000 | 20% | 20% | 20% | 5% |

| ₹6,00,001 – ₹7,00,000 | 20% | 20% | 20% | 5% |

| ₹7,00,001 – ₹7,50,000 | 20% | 20% | 20% | 10% |

| ₹7,50,001 – ₹9,00,000 | 20% | 20% | 20% | 10% |

| ₹9,00,001 – ₹10,00,000 | 20% | 20% | 20% | 10% |

| ₹10,00,001 – ₹12,00,000 | 30% | 30% | 30% | 15% |

| ₹12,00,001 – ₹12,50,000 | 30% | 30% | 30% | 20% |

| ₹12,50,001 – ₹15,00,000 | 30% | 30% | 30% | 20% |

| ₹15,00,000 and above | 30% | 30% | 30% | 30% |

- Salary income: The standard deduction of ₹50,000, which was only available under the old regime, has now been extended to the new tax regime as well. This amount has been increased to ₹75,000 for the new regime only with effect from FY 2024-25.

- Family pension: Those receiving a family pension can claim a deduction of ₹15,000 or 1/3rd of the pension, whichever is lower. This amount has been increased to ₹25,000 for the new regime with effect from FY 2024-25.

- Reduced Surcharge for High Net Worth Individuals: The surcharge rate on income over ₹5 crores has been reduced from 37% to 25%. This move will bring down their effective tax rate from 42.74% to 39%.

- Higher Leave Encashment Exemption: The exemption limit for non-government employees has been raised from ₹3 lakhs to ₹25 lakhs, an 8-fold increase.

- Default Regime: Starting from FY 2023-24, the new income tax regime will be set as the default option. If you want to continue using the old regime, you must submit the income tax return along with Form 10-IEA before the due date. You will have the option to switch between the two regimes annually to check the tax benefits.

3. What Deductions and Exemptions are Allowed Under the New Tax Regime?

Here is a quick insight into the comparison between the deductions and exemptions available under the new and the old tax regime:

| Particulars | Old Tax Regime | New tax Regime (until 31st March 2023) | New Tax Regime (FY 2023-24) | New Tax Regime (FY 2024-25) |

| Income level for rebate eligibility | ₹ 5 lakhs | ₹ 5 lakhs | ₹ 7 lakhs | ₹ 7 lakhs |

| Standard Deduction | ₹ 50,000 | – | ₹ 50,000 | ₹ 75,000 |

| Effective Tax-Free Salary income | ₹ 5.5 lakhs | ₹ 5 lakhs | ₹ 7.5 lakhs | ₹ 7.75 lakhs |

| Rebate u/s 87A | ₹12,500 | ₹12,500 | ₹25,000 | ₹25,000 |

| HRA Exemption | ✓ | X | X | X |

| Leave Travel Allowance (LTA) | ✓ | X | X | X |

| Other allowances including food allowance of Rs 50/meal subject to 2 meals a day | ✓ | X | X | X |

| Standard Deduction | ✓ | X | ✓ | ✓ |

| Entertainment Allowance and Professional Tax | ✓ | X | X | X |

| Perquisites for official purposes | ✓ | ✓ | ✓ | ✓ |

| Interest on Home Loan u/s 24b on: Self-occupied or vacant property | ✓ | X | X | X |

| Interest on Home Loan u/s 24b on: Let-out property | ✓ | ✓ | ✓ | ✓ |

| Deduction u/s 80C (EPF | LIC | ELSS | PPF | FD | Children’s tuition fee etc) | ✓ | X | X | X |

| Employee’s (own) contribution to NPS | ✓ | X | X | X |

| Employer’s contribution to NPS | ✓ | ✓ | ✓ | ✓ |

| Medical insurance premium – 80D | ✓ | X | X | X |

| Disabled Individual – 80U | ✓ | X | X | X |

| Interest on education loan – 80E | ✓ | X | X | X |

| Interest on Electric vehicle loan – 80EEB | ✓ | X | X | X |

| Donation to Political party/trust etc – 80G | ✓ | X | X | X |

| Savings Bank Interest u/s 80TTA and 80TTB | ✓ | X | X | X |

| Other Chapter VI-A deductions | ✓ | X | X | X |

| All contributions to Agniveer Corpus Fund – 80CCH | ✓ | Did not exist | ✓ | ✓ |

| Deduction on Family Pension Income | ✓ | X | ✓ | ✓ |

| Gifts upto Rs 50,000 | ✓ | ✓ | ✓ | ✓ |

| Exemption on voluntary retirement 10(10C) | ✓ | ✓ | ✓ | ✓ |

| Exemption on gratuity u/s 10(10) | ✓ | ✓ | ✓ | ✓ |

| Exemption on Leave encashment u/s 10(10AA) | ✓ | ✓ | ✓ | ✓ |

| Daily Allowance | ✓ | ✓ | ✓ | ✓ |

| Conveyance Allowance | ✓ | ✓ | ✓ | ✓ |

| Transport Allowance for a specially-abled person | ✓ | ✓ | ✓ | ✓ |

4. Tax under Old vs New Regime for FY 2024-25

Here are a few calculations that will help you decide between the old vs the new tax regime:

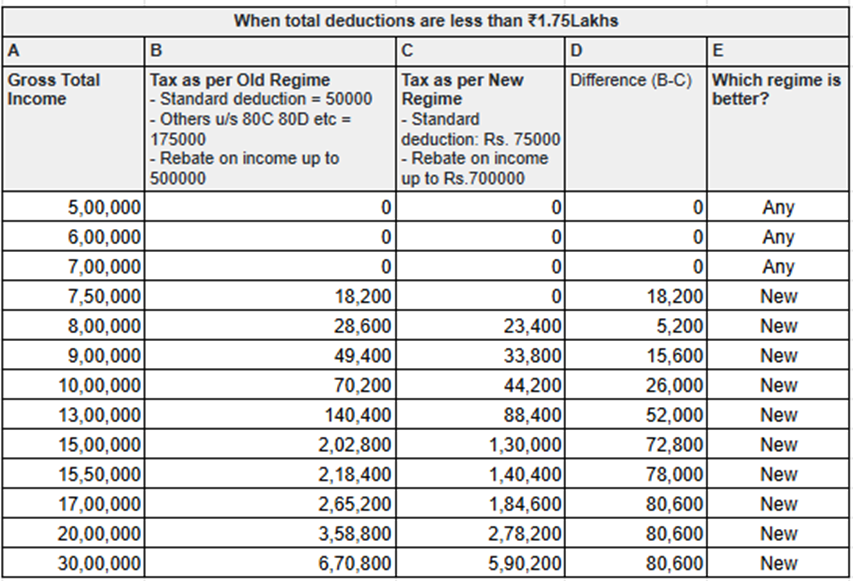

- When your gross total income is up-to Rs.7,00,000 (before Chapter VI-A Deductions and Standard Deduction) and you have Chapter VI A deduction of Rs.1,75,000, you won’t be taxed under any of the regimes. So you can file under old or new tax regime.

- When your gross total income is greater than Rs.7,00,000 (before Chapter VI-A Deductions and Standard Deduction) and total Chapter VI A deductions are ₹1.75 lakhs or less: The new regime will be beneficial.

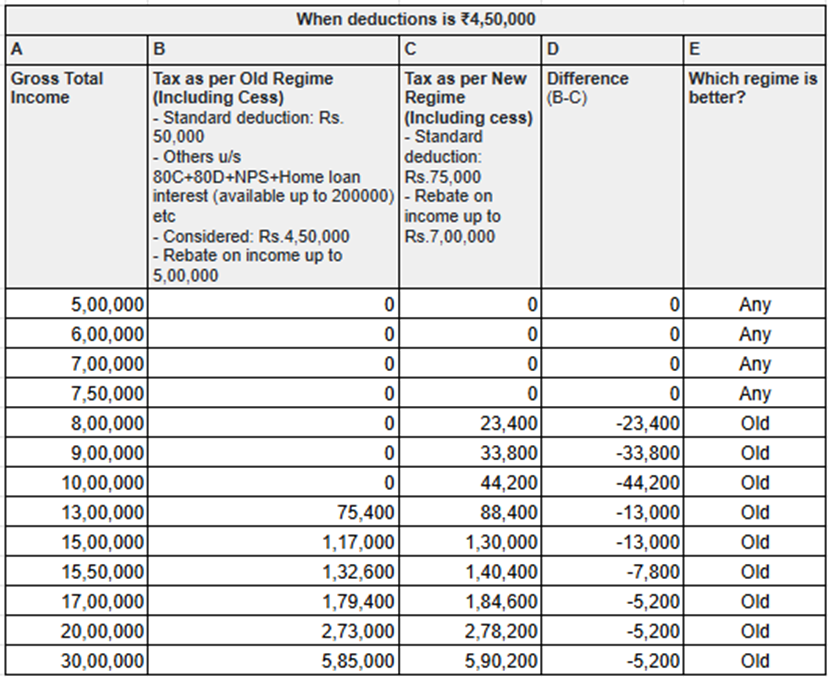

- When total deductions are more than ₹4.5 : The old regime will be beneficial.

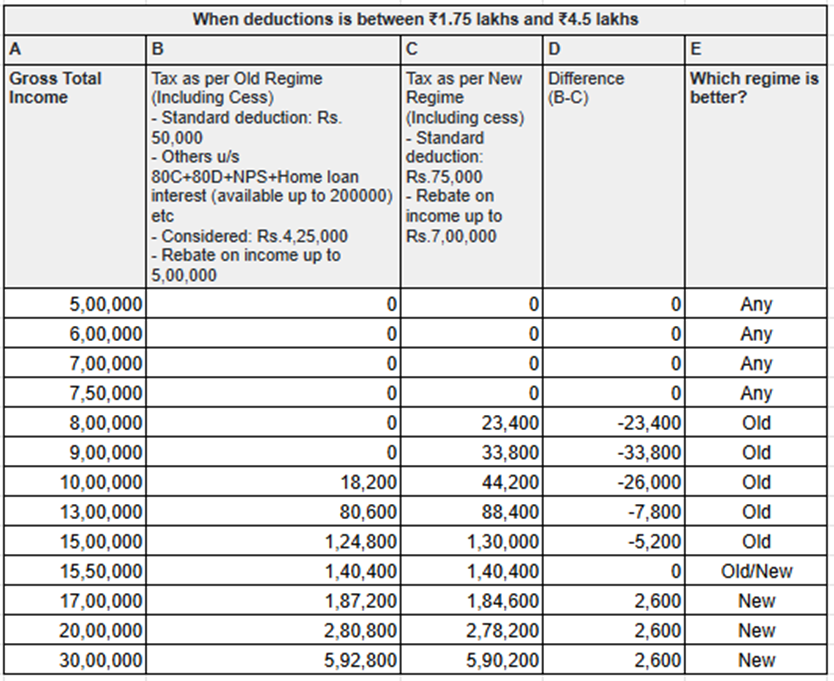

- When total deductions are between ₹1.75 lakhs to ₹4.5 lakhs: Will depend on your income level.

A. When Total Deductions are ₹1.75 Lakhs or Less: The New Tax Regime will be Beneficial

B. When Total Deductions are More Than ₹ 4.5 Lakhs: The Old Tax Regime will be Beneficial

C. When Total Deductions are Between ₹1.75 Lakhs to ₹4.5 Lakhs: Will Depend on Various Income Levels

Conclusion:

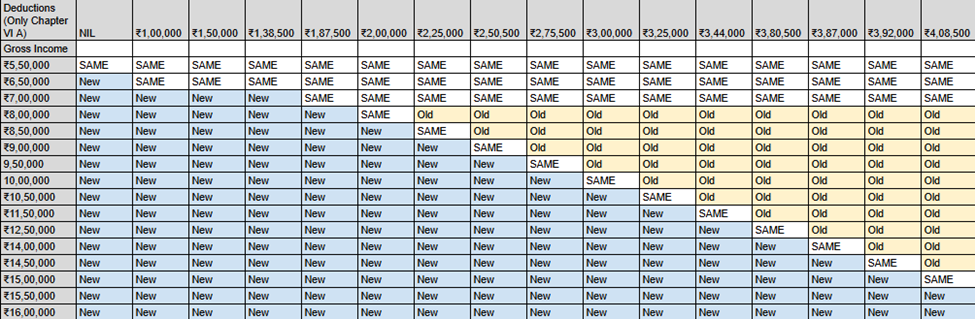

The decision to switch to the new or remain in the old tax regime or which regime is better for you shall be based on the tax savings deductions and exemptions you are eligible for in the old tax regime. To make it easier, we have calculated a breakeven point for various income levels (refer to the table below) for a salaried individual below 60 years of age. This can be used to determine which regime to choose.

The table below shows which tax regime is more beneficial at various income levels and deduction amounts.

If you have Salary Income: