TATA AIG Medicare Premier is a simplified and comprehensive Health Insurance plan.

Tata AIG General Insurance Company Limited (We, Our or Us) will provide the insurance cover, described in this Policy and any endorsements thereto, for the Insured Period, as defined in the Policy schedule. The insurance cover provided under this Policy is only with respect to such and so many of the benefitsupto the Sum Insured as mentioned in the Policy Schedule. Commencement of risk cover under the policy is subject to receipt of premium by us.

The statements and declarations contained in the Proposal signed by the Policyholder (You) and/or medical reports shall be the basis of this Policy and are deemed to be incorporated herein. The insurance cover is governed by and subject to, the terms, conditions and exclusions of this Policy.

Customer Obligations:

Please disclose all pre-existing disease/s or condition/s before buying a policy. Non-disclosure may result in claim not being paid and termination of Your policy.

The premiums are calculated after taking into account your age, your location (zonal), your medical condition, (any pre-existing diseases), and lifestyle habits (smoking, drinking, etc.)

Do any member(s) have any existing illnesses for which they take regular medication?

Diabetes

Blood Pressure

Heart disease

Any Surgery

Thyroid

Asthma

Other disease

Preamble

While the policy is in force, if the Insured Person contracts any disease or suffers from any illness or sustains bodily injury through accident and if such event requires the insured Person to incur expenses for Medically Necessary Treatment, We will indemnify You for the amount of such Reasonable and Customary Charges or compensate to the extent agreed, upto the limits mentioned, subject to terms and conditions of the Policy. Each Benefit is subject to its Sum Insured, but Our liability to make payment in respect of any and all Benefits shall be limited to the Sum Insured unless expressly stated to the contrary.

In case of family floater policy, the sum insured for all or any of the benefits shall be on a per policyper year basis unless explicitly stated to the contrary.

In case of an individual policy, the sum insured for all or any of the benefits shall be on a per insured per year basis unless explicitly stated to the contrary.

The said Medically Necessary Treatmentmust be on the advice of a qualified Medical Practitioner.

Suitability:

a. This policy covers persons in the age group 91 days onwards (Dependent children between 91 days and 5 years can be insured only when both parents are getting insured). The maximum entry age is 65 years. ( Adult: 18 – 65 & Child: 91Days – 25)

b. There is no maximum cover ceasing age under this policy. (Life long renewal)

c. The policy will be issued for a period 1/2/3 years.

d. This policy can be issued to an individual and/or family(1 – 7)

e. The family includes spouse and economically dependent children and parents/parents-in- law.

f. The policy offers coverage on family floater basis.

g. Maximum 7 members of a family are covered in one Individual Plan Policy (Self, spouse, 3 dependent children , 2 parents and 2 parent-in-laws ).

h. Maximum 7 members are covered in one Family Floater Plan policy (Self, spouse, 3 dependent children (Up to the age of 25 Years) , 2 parents and 2 parent-in-laws. In case of family floater, where age of the dependent child is crossing 25 years, the child can be covered under a separate policy with eligible continuity benefit.

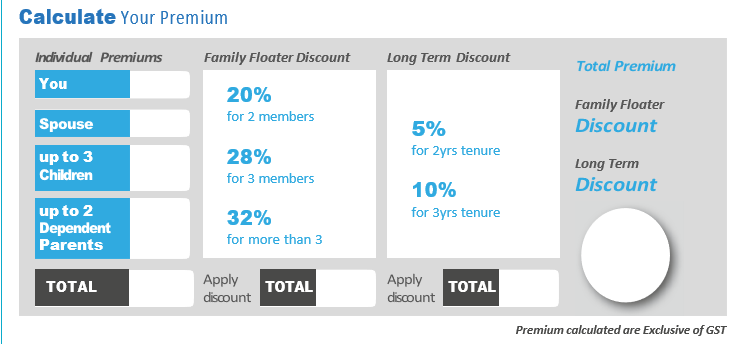

i. Discount

Family Discount:

20% for 2 members.

28% for upto 3 members.

32% for more than 3 members.

Long Term Discount:

5% for 2 years.

10% for 3 years.

Sum Insured options (Rs.) :

5 Lacs

10 Lacs

15 Lacs

20 Lacs

25 Lacs

50 Lacs

75 Lacs

100 Lacs

200 Lacs

300 Lacs (3Crore)

Type of Insurance Policy

Both indemnity & benefit, Policy has elements of both, Indemnity (which cover insured loses) and Benefit (which pays a fix amount under the policy on the occurrence of a covered event).

Zone(s) – (Different for Select and Premier)

For the purpose of premium computation, the country is divided into following three Zones and premium payable under the policy will be computed based on the residential location/address as provided by the proposer/insured person in the proposal form:

Zone A: Mumbai (including Mumbai Metropolitan Region), Delhi (including National Capital Region, Faridabad, Ghaziabad), Ahmedabad, Surat & Baroda

Zone B: Hyderabad (including Secunderabad), Bengaluru, Kolkata, Indore, Chennai, Chandigarh (including, Mohali, Punchkula, Zirakpur), Pune (including Pimpri Chinchwad) and Rajkot

Zone C: Rest of India

Please note that the above-mentioned categorization of zones is subject to change at Our sole discretion. Any such change made which shall impact an existing policyholder, shall be intimated under 3 months’ notice and shall be applicable from the immediate next renew

Lifelong renewal:

We offer you a lifelong renewal for your policy provided premium is paid without any break. Your premiums will be basis the age, sum insured, zone, optional cover(s) and applicable discounts, if any. Your renewal premium will be basis your age on renewal and applicable discounts, if any. There will be no extra loadings based on your individual claim.

The policy is renewable except in the case of established fraud or non-disclosure or misrepresentation by the Insured Person.

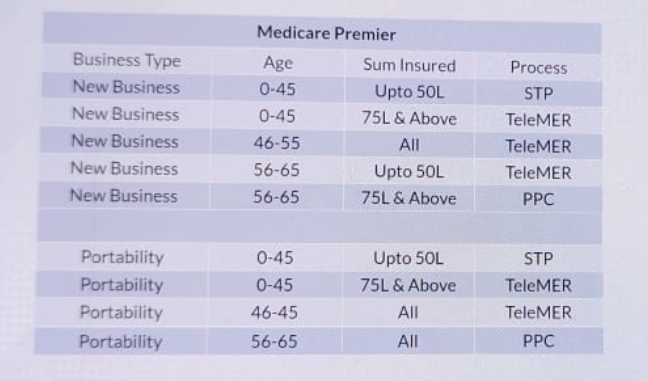

Pre-Policy Check-up (PPC)

Pre-Policy Check-up at our network is required. The medical reports are valid for a period of 90 days from the date of the Pre-Policy Check-up. The company may conduct Tele MER/Video, MER/Pre-Policy Check-up based on age/Sum Insured medical declaration or any other underwriting criteria. 100% of the expenses incurred per insured person will be payable by Tata AIG only on the acceptance of the proposal.

In case of an adverse medical declaration, we may call for additional medical tests. We may conduct medical tests at diagnostic centres based on medical disclosure wherever applicable. At least 50% of the Pre-Policy medical Check-up cost would be borne by TATA AIG in case a Pre-Policy Check-up (PPC) is conducted and the proposal is accepted.

Pre-policy medical examination gird:

Age(Yrs)/Sum Insured

Sum Insured up to Rs.50 Lacs

Sum Insured above Rs.50 Lacs

Upto age 45

Tele MER (only if positive medical declaration)

Tele MER

46-55

Tele MER

Tele MER

56 to 65

Tele MER

*MER, Urine Routine, CBC with ESR, LFT, RFT, Lipid Profile, TMT/ (2D Echo+ECG), USG Abdomen & Pelvis, Hba1c, HBsAg, X ray chest, Sonomammography (female), PSA (male)

In case of adverse medical declaration, we may call for TeleMER/additional medical tests

Tele-MER means Tele Medical Examination Reporting.

100% of TeleMER cost would be borne by the Company, in case of proposal acceptance.

*At least 50% of pre-policy medical checkup cost would be borne by the Company in case where proposal is accepted.

Financial underwriting may be done in case of higher sum insured options.

Section 1 – General Definitions

The terms defined below and at other junctures in the Policy Wording have the meanings ascribed to them wherever they appear in this Policy and, where appropriate, references to the singular include references to the plural; references to the male include the female and third gender, references to any statutory enactment include subsequent changes to the same:

Standard Definitions

1. Accident

An accident means sudden, unforeseen and involuntary event caused by external, visible and violent means.

2. Any one illness

Any one illness means continuous period of illness and includes relapse (the return of a disease) within 45 days from the date of last consultation with the Hospital/Nursing Home where treatment was taken.

3. AYUSH Day Care Centre

AYUSH Day Care Centre means and includes Community Health Centre (CHC), Primary Health Centre (PHC), Dispensary, Clinic, Polyclinic or any such health centre which is registered with the local authorities, wherever applicable and having facilities for carrying out treatment procedures and medical or surgical/para-surgical interventions or both under the supervision of registered AYUSH Medical Practitioner (s) on day care basis without in-patient services and must comply with all the following criterion:

Having qualified registered AYUSH Medical Practitioner(s)in charge;

Having dedicated AYUSH therapy sections as required and/or has equipped operation theatre where surgical procedures are to be carried out;

Maintaining daily records of the patients and making them accessible to the insurance company’s authorized representative.

4. AYUSH Hospital

An AYUSH Hospital is a healthcare facility wherein medical/surgical/para-surgical treatment procedures and interventions are carried out by AYUSH Medical Practitioner(s) comprising of any of the following:

Central or State Government AYUSH Hospital or

Teaching hospital attached to AYUSH college recognized by the Central Government/ Central Council of Indian Medicine/ Central Council for Homeopathy, or

AYUSH Hospital, standalone or co-located with in-patient healthcare facility of any recognized system of medicine, registered with the local authorities, wherever applicable, and is under the supervision of a qualified registered AYUSH Medical Practitioner and must comply with all the following criterion:

Having atleast 5 in-patient beds;

Having qualified AYUSH Medical Practitioner round the clock;

Having dedicated AYUSH therapy sections as required and/or has equipped operation theatre where surgical procedures are to be carried out

Maintaining daily records of the patients and making them accessible to the insurance company’s authorized representative.

5. AYUSH Treatment

AYUSH treatment refers to the medical and / or hospitalization treatments given under Ayurveda, Yoga and Naturopathy, Unani, Siddha and Homeopathy systems.

6. Break in Policy

Break in policy means the period of gap that occurs at the end of the existing policy term/instalment premium due date, when the premium due for renewal on a given policy or instalment premium due is not paid on or before the premium renewal date or grace period.

7. Cashless facility

Cashless facility means a facility extended by the insurer to the insured where the payments, of the costs of treatment undergone by the insured in accordance with the policy terms and conditions, are directly made to the network provider by the insurer to the extent pre-authorization is approved.

8. Condition Precedent

Condition Precedent means a policy term or condition upon which the Insurer’s liability under the policy is conditional upon.

9. Congenital Anomaly:

Congenital Anomaly means a condition which is present since birth, and which is abnormal with reference to form, structure or position.

a) Internal Congenital Anomaly

Congenital anomaly which is not in the visible and accessible parts of the body.

b) External Congenital Anomaly

Congenital anomaly which is in the visible and accessible parts of the body

10. Cumulative Bonus /No Claim Discount:

Cumulative Bonus means any increase or addition in the Sum Insured granted by the insurer without an associated increase in premium.

11. Day Care Centre

A day care centre means any institution established for day care treatment of illness and/or injuries or a medical setup with a hospital and which has been registered with the local authorities, wherever applicable, and is under supervision of a registered and qualified medical practitionerAND must comply with all minimum criterion as under –

has qualified nursing staff under its employment;

has qualified medical practitioner/s in charge;

has fully equipped operation theatre of its own where surgical procedures are carried out;

maintains daily records of patients and will make these accessible to the insurance company’s authorized personnel.

12. Day Care Treatment

Day care treatment means medical treatment, and/or surgical procedure which is:

undertaken under General or Local Anesthesia in a hospital/day care centre in less than 24 hrs because of technological advancement, and

which would have otherwise required hospitalization of more than 24 hours.

Treatment normally taken on an out-patient basis is not included in the scope of this definition

13. Dental Treatment

Dental treatment means a treatment related to teeth or structures supporting teeth including examinations, fillings (where appropriate), crowns, extractions and surgery.

14. Domiciliary Hospitalization

Domiciliary hospitalization means medical treatment for an illness/disease/injury which in the normal course would require care and treatment at a hospital but is actually taken while confined at home under any of the following circumstances:

the condition of the patient is such that he/she is not in a condition to be removed to a hospital, or

the patient takes treatment at home on account of non-availability of room in a hospital.

15. Grace Period

“Grace period” means the specified period of time, immediately following the premium due date during which premium payment can be made to renew or continue a policy in force without loss of continuity benefits pertaining to waiting periods and coverage of pre-existing diseases.

For single premium payment policies, coverage is not available during the period for which no premium is received. However, If the premium is paid in instalments during the policy period, coverage will be available during the grace period, within the policy period.

The grace period for payment of the premium shall be:fifteen days where premium payment mode is monthly and thirty days in all other cases.

16. Hospital

A hospital means any institution established for in-patient care and day care treatment of illness and/or injuries and which has been registered as a hospital with the local authorities under Clinical Establishments (Registration and Regulation) Act 2010 or under enactments specified under the Schedule of Section 56(1) and the said act Or complies with all minimum criteria as under:

has qualified nursing staff under its employment round the clock;

has at least 10 in-patient beds in towns having a population of less than 10,00,000 and at least 15 in-patient beds in all other places;

has qualified medical practitioner(s) in charge round the clock;

has a fully equipped operation theatre of its own where surgical procedures are carried out;

maintains daily records of patients and makes these accessible to the insurance company’s authorized personnel;

17. Hospitalization

Hospitalization means admission in a Hospital for a minimum period of 24 consecutive ‘In- patient Care’ hours except for specified procedures/ treatments, where such admission could be for a period of less than 24 consecutive hours.

18. Illness

Illness means a sickness or a disease or pathological condition leading to the impairment of normal physiological function and requires medical treatment.

a) Acute condition

Acute condition is a disease, illness or injury that is likely to respond quickly to treatment which aims to return the person to his or her state of health immediately before suffering the disease/ illness/ injury which leads to full recovery

b) Chronic condition

A chronic condition is defined as a disease, illness, or injury that has one or more of the following characteristics:

it needs ongoing or long-term monitoring through consultations, examinations, check- ups, and /or tests

it needs ongoing or long-term control or relief of symptoms

it requires rehabilitation for the patient or for the patient to be specially trained to cope with it

it continues indefinitely

it recurs or is likely to recur

19. Injury

Injury means accidental physical bodily harmexcluding illness or disease solely and directly caused by external, violent, visible and evident means which is verified and certified by a Medical Practitioner.

20. Inpatient Care

Inpatient care means treatment for which the insured person has to stay in a hospital for more than 24 hours for a covered event.

21. Maternity expenses

Maternity expenses means;

medical treatment expenses traceable to childbirth (including complicated deliveries and caesarean sections incurred during hospitalization);

expenses towards lawful medical termination of pregnancy during the policy period.

22. Medical Advice

Medical Advice means any consultation or advice from a Medical Practitioner including the issuance of any prescription or follow-up prescription.

23. Medical Expenses:

Medical Expenses means those expenses that an Insured Person has necessarily and actually incurred for medical treatment on account of Illness or Accident on the advice of a Medical Practitioner, as long as these are no more than would have been payable if the Insured Person had not been insured and no more than other hospitals or doctors in the same locality would have charged for the same medical treatment.

24. Medical Practitioner

Medical Practitioner means a person who holds a valid registration from the Medical Council of any State or Medical Council of India or Council for Indian Medicine or for Homeopathy set up by the Government of India or a State Government and is thereby entitled to practice medicine within its jurisdiction; and is acting within its scope and jurisdiction of license.

25. Medically Necessary Treatment

Medically necessary treatment means any treatment, tests, medication, or stay in hospital or part of a stay in hospital which:

is required for the medical management of the illness or injury suffered by the insured;

must not exceed the level of care necessary to provide safe, adequate and appropriate medical care in scope, duration, or intensity;

must have been prescribed by a medical practitioner;

must conform to the professional standards widely accepted in international medical practice or by the medical community in India.

26. Migration

“Migration” means a facility provided to policyholders (including all members under family cover and group policies), to transfer the credits gained for pre-existing diseases and specific waiting periods from one health insurance policy to another with the same insurer.

27. Network Provider

Network Provider means hospitals or health care providers enlisted by an insurer, TPA or jointly by an Insurer and TPA to provide medical services to an insured by a cashless facility.

The updated list of Network Provider is available on Our website (www.tataaig.com).

28. New Born Baby

Newborn baby means baby born during the Policy Period and is aged upto 90 days

29. Notification of Claim

Notification of claim means the process of intimating a claim to the insurer or TPA through any of the recognized modes of communication.

30.OPD treatment

OPD treatment means the one in which the Insured visits a clinic / hospital or associated facility like a consultation room for diagnosis and treatment based on the advice of a Medical Practitioner. The Insured is not admitted as a day care or in-patient.

31. Pre-Existing Disease

“Pre-existing disease (PED)” means any condition, ailment, injury or disease:

that is/are diagnosed by a physician not more than 36 months prior to the date of commencement of the policy issued by the insurer; or

for which medical advice or treatment was recommended by, or received from, a physician, not more than 36 months prior to the date of commencement of the policy.

32. Pre-hospitalization Medical Expenses

Pre-hospitalization Medical Expenses means medical expenses incurred during predefined number of days preceding the hospitalization of the Insured Person, provided that:

Such Medical Expenses are incurred for the same condition for which the Insured Person’s Hospitalization was required, and

The In-patient Hospitalization claim for such Hospitalization is admissible by the Insurance Company.

33. Portability

“Portability” means a facility provided to the health insurance policyholders (including all members under family cover), to transfer the credits gained for, pre-existing diseases and specific waiting periodsfrom one insurer to another insurer.

Requirement:

Completed proposal form,

Supporting Medical papers (wherever applicable),

Previous policy copies, IRDAI portability form (as applicable)

34. Post-hospitalization Medical Expenses

Post-hospitalization Medical Expenses means medical expenses incurred during predefined number of days immediately after the insured person is discharged from the hospital provided that:

Such Medical Expenses are for the same condition for which the insured person’s hospitalization was required, and

The inpatient hospitalization claim for such hospitalization is admissible by the insurance company

35. Qualified Nurse

Qualified nurse means a person who holds a valid registration from the Nursing Council of India or the Nursing Council of any state in India.

36. Reasonable and Customary Charges

Reasonable and Customary charges means the charges for services or supplies, which are the standard charges for the specific provider and consistent with the prevailing charges in the geographical area for identical or similar services, taking into account the nature of the illness / injury involved.

37. Renewal

Renewal means the terms on which the contract of insurance can be renewed on mutual consent with a provision of grace period for treating the renewal continuous for the purpose of gaining credit for pre-existing diseases, time-bound exclusions and for all waiting periods.

38. Room Rent

Room Rent means the amount charged by a Hospital towards Room and Boarding expenses and shall include the associated medical expenses.

39. Surgery or Surgical Procedure

Surgery or Surgical Procedure means manual and / or operative procedure (s) required for treatment of an illness or injury, correction of deformities and defects, diagnosis and cure of diseases, relief from suffering and prolongation of life, performed in a hospital or day care centre by a medical practitioner.

40. Unproven/Experimental treatment

Unproven/Experimental treatment means the treatment including drug experimental therapy which is not based on established medical practice in India, is treatment experimental or unproven.

Specific Definitions (Definitions other than as mentioned under Section 1 (i)above)

1. Age

Means the completed age of the Insured Person on his / her most recent birthday as per the English calendar, regardless of the actual time of birth.

2. Policy

Policy means the contract of insurance including but not limited to Policy Schedule, Endorsements and Policy Wordings.

3. Policy period

Policy Period means the time during which this Policy is in effect. Such period commences from Commencement Date and ends on the Expiry Date and specifically appears in the Policy Schedule.

4. Policy Schedule

Policy Schedule means the Policy Schedule attached to and forming part of Policy

5. Policy year

Policy Year means a period of twelve months beginning from the date of commencement of the Policy period and ending on the last day of such twelve-month period. For the purpose of subsequent years, policy year shall mean a period of twelve months commencing from the end of the previous policy year and lapsing on the last day of such twelve-month period, till the Policy Expiry date

6. Shared Accommodation

Shared Accommodation means a hospital room with two or more patient beds. This definition does not apply to ICU or ICCU.

Section 2 – Benefits

Below listed benefits are payable subject to Terms and Conditions of the policy.

The company’s maximum liability in aggregate for payment of any claim under Section B1, B2, B3, B4 and B7 shall not exceed the opted sum insured. However, any payment under cumulative bonus shall be over and above.

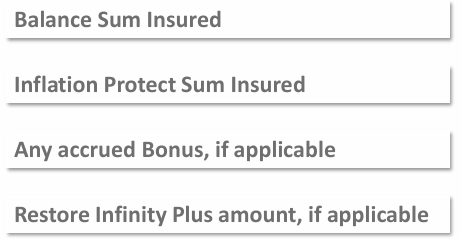

The sequence of utilization of benefits for a claim shall be as per the following:

Sum Insured,

Any accrued Cumulative Bonus, if applicable

Restore benefit amount, if applicable

B1. In-Patient Treatment

We will cover for expenses for hospitalization due to disease/illness/Injury during the policy period that requires an Insured Person’s admission in a hospital as an inpatientfor period more than 24 hrs.

Medical expenses directly related to the hospitalization would be payable.

Benefit Specific Sub-limit: In-Patient Treatment- Upto Sum Insured

B2. Pre-Hospitalization expenses

We will cover for expenses for Pre-Hospitalization consultations,investigations and medicines incurredupto 60 days before the date of admission to the hospital.

The benefit is payable if We have admitted a claim under section B1 or B4 or B6 or B31 of this policy.

Benefit Specific Sub-limit: Pre-Hospitalization expenses – Up to 60 days, Up to Sum Insured

B3. Post-Hospitalization expenses

We will cover for expenses for Post-Hospitalization consultations, investigations and medicines incurred after discharge from the hospital, upto number of days as specified in the table below.

Basic Sum insured

Number of days

Upto Rs. 50 Lacs

90 days Upto Sum Insured

Rs.75 Lacs to Rs.3 Crore

200 days, Upto Sum Insured

In case the insured person has opted sum insured Rs. 75 Lacs and above, then We will arrange up to 15 physiotherapy sessions at home within India, wherever available, within the city in which you reside through our empanelled service provider subject to following conditions:

This limit on physiotherapy sessions is applicable to each insured person, per post- hospitalization event

Availing the services for physiotherapy at home under this Benefit is at insured person’s sole discretion and risk. We do not assume any liability towards quality of service rendered, any immediate or consequential loss arising out of or in relation to these services rendered by the empanelled service provider.

The said physiotherapy must be advised in writing by the treating medical practitioner.

The above services may be provided by the company /network providers or other empaneled hospitals / service providers. Any additional expenses other than the eligible expenses shall be borne by the insured person which shall not be covered under this policy unless specified otherwise

This facility may be availed through our website or our mobile application or through calling our call centre on the toll free number specified in the policy schedule. Alternatively, details of our empanelled service provider are available on our website (www.tataaig.com)

In case we or the empanelled service provider fails to provide any of the services as mentioned in this policy or is unable to implement , in whole or in part due to force majeure, non-availability of services, change in law, rule or regulations which affects the services, or if any regulatory or governmental agency having jurisdiction over a party takes a position which affects the services, then the service provider services suspended, curtailed or limited performance shall not constitute breach of contract and the company or the empanelled service provider shall have no liability whatsoever including but not limited to any immediate or consequential loss resulting therefrom.

The benefit is payable if We have admitted a claim under section B1 or B4 or B6 or B31 of this policy.

B4. Day Care Procedures

Day care treatment means medical treatment, and/or surgical procedure which is:

undertaken under General or Local Anesthesia in a hospital/day care centre in less than 24 hrs because of technological advancement, and

which would have otherwise required hospitalization of more than 24 hours.

We will cover expenses for Day Care Treatment (541)due to disease/illness/Injury during the policy period taken at a hospital or a Day Care Centre.

Benefit Specific Sub-limit: Day Care Procedures- Upto Sum Insured

Treatment normally taken on out-patient basis is not included in the scope of this cover.

We will cover for Medical and surgical Expenses of the organ donor for harvesting the organ where an Insured Person is the recipientprovided that:

The organ donor is any person whose organ has been made available in accordance and in compliance with The Transplantation of Human Organs (Amendment) Bill, 2011 and the organ donated is for the use of the Insured Person, and

We have accepted an inpatient Hospitalization claim for the insured member under section B1 of this policy.

Benefit Specific Sub-limit: – Upto Sum Insured

B6. Domiciliary Treatment

Medical Expenses incurred for availing medical treatment at home which would otherwise have required hospitalization. We will also cover pre and post hospitalization expenses in case of domiciliary hospitalization.

We will cover for expenses related to Domiciliary Hospitalization of the insured person if the treatment exceeds beyond three days. The treatment must be for management of an illness and not for enteral feedings or end of life care.

At the time of claiming under this benefit, we shall require certification from the treating doctor fulfilling the conditions as mentioned under the general definitions (Section 1) of this policy.

Benefit Specific Sub-limit: – Upto Sum Insured

Domiciliary hospitalization means medical treatment for an illness/disease/injury which in the normal course would require care and treatment at a hospital but is actually taken while confined at home under any of the following circumstances:

the condition of the patient is such that he/she is not in a condition to be removed to a hospital, or

the patient takes treatment at home on account of non-availability of room in a hospital.

B7. Restore Benefit

We will automatically restore the Basic Sum Insuredif the Sum Insured and accrued Cumulative Bonus is insufficient to pay a claim during the policy year. This benefit can be availed once during the policy year subject to the following conditions:

The restored sum insured can be used for any admissible claim under Sections B1 to B4, for the insured person(s) who have not claimed earlier under these Sections. In case the insured has claimed under these sections, then this automatic restoration benefit is available for admissions due to unrelated illness/diseases. However, this benefit for related illness/diseases would be available, in case of claimed insured person(s), for admissions after 45 days from the date of discharge of the earlier claim. (now this 45 days not applicable)

In case of Family Floater policy, Reinstatement of Sum Insured will be available for all Insured Persons in the Policy on floater basis.

For policy with Basic Sum Insured less than or Equal to Rs. 50 Lacs: This benefit shall be applicable annually for policies with tenure of more than 1 year.

For policy with Basic Sum Insured Rs. 75 Lacs and above: This benefit shall be applicable annually for multiyear policies. However, for single premium multiyear policies, the insured shall have the right to utilize the available restorations anytime during the policy period, except for the first claim, for

e.g. a policy with tenure of 2 years where entire premium is paid upfront, the insured is eligible for a total of 2 restorations anytime during the policy period except for the first claim in each policy year.

d. The unutilized restored sum insured cannot be carried forward to the next policy year.

e. Restore will not trigger for the first claim under each policy year.

f. The maximum liability under a single claim under this benefit shall be the sum Insured.

This benefit shall not be available for section B13 and B31 of this policy.

Benefit Specific Sub-limit:– Upto Sum Insured

Restore — full and partial but TATA is partially which is best ….most of the companies are giving Full restoration..

B8. AYUSH Benefit

We will cover Medical Expenses incurred for treatment as In-Patient or Day Care Treatment costs incurred under Ayurveda, Yoga and Naturopathy, Unani, Sidha or Homoeopathy will be covered in an AYUSH Hospital/ AYUSH day care centre.

Benefit Specific Sub-limit: – Upto Sum Insured

This benefit shall also cover Pre-Hospitalization medical expenses for a period of upto 60 days before the date of admission to the AYUSH hospital/ AYUSH day care centre and Post-Hospitalization Medical Expenses for a period upto number of days as specified in the table below, subject to AYUSH In-Patient hospitalization or AYUSH day care treatment claim being admissible under this benefit.

We will cover for expenses incurred on transportation of Insured Person in a registered ambulance to a Hospital for admission in case of an Emergency or from one hospital to another hospital for better medical facilities and treatment, subject to limited as specified in the table below.

Basic Sum Insured

Sub Limit (not for whole year)

Up to Rs. 50 Lacs

Upto Rs. 5000 per hospitalization

Rs. 75 Lacs

Upto Rs. 7500 per hospitalization

Rs. 1 Crore

Upto Rs. 10000 per hospitalization

Rs. 2 Crore

Upto Rs. 20000 per hospitalization

Rs. 3 Crore

Upto Rs. 30000 per hospitalization

For this claim to be paid, the claim must be admissible under section B1 or B4 of this policy.

B10. Health Checkup (must use)

We will cover for expenses for a Preventive Health Check-up upto 1% of policy sum insured subject to a maximum limit as specified in the table below. The limit is the maximum per policy in case of floater policy and per insured person in case of individual policy

The benefit is payable every year irrespective of claims under the policy. This benefit has a separate limit (over and above base sum insured) and does not affect cumulative bonus.

Basic Sum Insured (Rs.)

Sub Limit

Up to Rs. 50 Lacs

Upto Rs. 10000

Rs. 75 Lacs

Upto Rs. 15000

Rs. 1 Crore

Upto Rs. 20000

Rs. 2 Crore

Upto Rs. 25000

Rs. 3 Crore

Upto Rs. 25000

General Note: Preventive health check only cashless from first year onwards….1 MG team will come and collect samples at home…

For the purpose of this benefit, Preventive Health Check-up means medical test(s) undertaken for general assessment of health status and does not include any diagnostic or investigative medical tests for evaluation of illness or a disease.

B11. Compassionate travel

a. Domestic(During any Visit to other place)

In the event the Insured Person is Hospitalized in Indiafor more than Five consecutive days in a place where no adult member of his immediate family is present, we will cover for expenses related to a round trip economy class air ticket, or first-class railway ticket, to allow the Immediate Family Member be at his bedside for the duration of his stay in the hospital.

The benefit shall be payable if an inpatient Hospitalization claim for the insured member is admissible under section B1 of this Policy.

b. Global (Applicable for sum insured above Rs. 50 Lacs):

In the event the Insured person is hospitalized outside India and claim is admissible under section B13(Global cover for Planned Hospitalization) of this policy, We will cover expenses related to round trip economy class air ticket, to allow the Immediate Family Member to accompany the Insured person for the purpose of planned treatment outside India.

Note: insured person expenses will be coverd in B13, here only for family member.

This benefit has a separate limit (over and above base sum insured) as specified in the policy schedule and does not affect cumulative bonus. We shall require the following additional documents (proof of travel) supporting the claim under this benefit:

Copy of Passport (in case of Global),

Boarding Pass, or Railway ticket or any other document to show proof of travel.

Basic Sum Insured (Rs.)

sub Limit

Up to Rs. 50 Lacs

Upto Rs.20,000 per policy year

Rs. 75 Lacs to Rs. 3 Crore

Upto Rs.50,000 per policy year

B12. Consumables Benefit

We will pay for expenses incurred, for specified consumables listed in ‘Annexure I – List I- Optional Items’ which are consumed during the period of hospitalization directly related to the insured’s medical or surgical treatment of illness/disease/injury. Details of Annexure I- List I-Optional items are available on our website (www.tataaig.com)

However, the following items shall be excluded from scope of this coverage:

Items of personal comfort, toiletries, cosmetics and convenienceshall be excluded from scope of this coverage.

External durable devices like Bilevel Positive Airway Pressure (BIPAP) machine, Continuous Positive Airway Pressure (CPAP) machine, Peritoneal Dialysis (PD) equipment and supplies, Nimbus/water/air bed, dialyzer and other medical equipments.

Any item which is neither medical consumable nor medically necessary nor prescribed by Doctor.

For this claim to be paid, the main claim must be admissible under section B1 or B4 or B31 of this policy..

Benefit Specific Sub-limit: Consumables Benefit Upto Sum Insured

B13. Global Cover for Planned Hospitalization

a. Global Cover for Planned Hospitalization (Medical Expenses)

Benefit Specific Sub-limit: Upto Sum Insured, For benefit applicable to you, please refer your Policy Schedule

We will cover for Medical Expenses(in patient & day care) of the Insured Person incurred outside India, upto the sum insured, provided that the diagnosis was made in India and the insured travels abroad for treatment.

The Medical Expenses payable shall be limited to Inpatient and daycare Hospitalization. Any claim under this cover can be made only on reimbursement basis. Cashless facility may be arranged on case to case basis. Insured person can contact us for claim assistance.

The payment of claim under this benefit will be in Indian Rupeesbased on the rate of exchange published by Reserve Bank of India (RBI), as on the date of invoice and shall be used for conversion of foreign currency into Indian Rupees for claims payment. If these rates are not published on the date of invoice, the exchange rate next published by RBI shall be considered for conversion.

Only the balance basic sum insured along with Cumulative Bonus can be used for this and not the restored sum insured.

We shall require the following additional documentssupporting the claim under this benefit:

Proof of diagnosis in India

Insured’s Passport and Visa

b. Visa Services Fees (Applicable only for Sum Insured above Rs.50 Lacs i.e 75lakh)

We will cover for reasonable and customary expenses incurred towards obtaining visa for medical treatment of the insured person (Only) travelling abroad upto the sum insured subject to claim being admissible under section B13 (a – Global Cover for Planned Hospitalization (Medical Expenses)) of this policy.

We shall require valid receipts/bills of visa fee services supporting the claim under this benefit.

Special condition applicable for cover B13 (a) & (b):

Please note that, B13. ‘Global Cover for Planned Hospitalization’ as a Benefit is:

a. not available under this policy and no claim shall be admissible under this section where either the policyholder or any of the Insured Person(s) is a Foreign National or their Residence Status at the time of proposal or anytime during the policy period/ renewal is:

Non-Resident Indian (NRI); or

Overseas Citizen of India (OCI)

b. not available under this Policy and no claim shall be admissible under this section, if the Policyholder or any of the Insured Person(s), as a Resident Indian National, has agreed to opt out of this Benefit at the time of proposal or at renewal.

If the coverage under B13. ‘Global Cover for Planned Hospitalization’ is once opted out, then neither the policyholder nor the Insured Person can take coverage under this benefit.

You are eligible for a premium discount @ 2% (once opted out) as specified in the prospectus in case this special condition, as mentioned above, is applicable to You/ Insured Person(s).

B14. Bariatric Surgery Cover

We’ll cover the cost of bariatric surgery to help deal with obesity and weight issues.

We will cover for reasonable and customary expenses for Bariatric Surgery if the insured fulfills all of the following conditions:

Surgery to be conducted is upon the advice of the Doctor

The member has to be 18 years of age or older and

Body Mass Index (BMI) greater than or equal to 40 or

BMI is greater than or equal to 35 in conjunction with any of the following severe co- morbidities following failure of less invasive methods of weight loss:

Obesity-related cardiomyopathy(a disease of the heart muscle)

Coronary heart disease

Severe sleep apnea

Uncontrolled Type2 Diabetes

In view of this coverage getting extended, exclusion code (Code-Excl06) of this policy stands deleted.

Limit : Bariatric Surgery Cover: Upto Sum Insured

B15. In-Patient Treatment – Dental

We will cover for medical expenses incurred towards hospitalization for dental treatment under anesthesia necessitated due to an accident/injury/illness.

Benefit Specific Sub-limit: In-Patient Treatment – Dental Upto Sum Insured

B16. Vaccination cover (must use)

We will cover for expenses related to the cost of the following vaccines only:

Basic Sum Insured

Vaccines covered

Up to Rs. 50 Lacs

Without any waiting period: 1. Anti-rabies vaccine following an animal bite 2. Typhoid vaccination

After 2 years of continuous coverage with Us: 1. Human Papilloma Virus (HPV) vaccine 2. Hepatitis B Vaccine

Rs. 75 Lacs to Rs. 3 Crore.

Without any waiting period: 1. Anti-rabies vaccine following an animal bite 2. Typhoid vaccination

After 2 years of continuous coverage with Us: 1. Human Papilloma Virus (HPV) vaccine 2. Hepatitis A Vaccine 3. Hepatitis B Vaccine 4. Tetanus, Diphtheria, Pertussis 5. Pneumococcal

Expenses related to the doctor, nurse or any incidental expenses are not payable. This benefit has a separate limit (over and above base sum insured) and does not affect cumulative bonus.

Limit : Vaccination cover: Upto Sum Insured (over and above base sum insured)

B17. Hearing Aid

The items must be prescribed by a specialized Medical Practitioner as medically necessary. This benefit has a separate limit (over and above base sum insured) and does not affect cumulative bonus.

We will cover for reasonable charges for a hearing aid every third year. The maximum amount (Sub Limit) payable is 50% of actual cost or Rs. 10,000/- per policy, whichever is lower.

B18. Daily Cash for choosing Shared Accommodation (no one will opt)

We will pay a fixed amount per day as mentioned in the policy schedule if the Insured Person is Hospitalized in Shared Accommodation in a Network Hospitalfor each continuous and completed period of 24 hours. The benefit payable per day would be (sub limit) 0.25% of base sum insured and a maximum of Rs. 2000 per day.(i.e 8lakhs above Rs.2000)

For this claim to be paid, the main claim must be admissible under section B1 of this policy. This benefit has a separate limit (over and above base sum insured) and does not affect cumulative bonus.

Limit for Daily Cash for choosing Shared Accommodation: Upto 0.25% of base sum insured and a maximum of ₹2000 per day. (over and above base sum insured)

B19. Daily Cash for Accompanying an Insured Child

We will pay a fixed amount per day, as mentioned in the policy schedule, if the Insured Person Hospitalized is a child Aged 12 years or less, for one accompanying adult for each complete period of 24 hours. The benefit payable per day would be (sub limit)0.25% of base sum insured and a maximum of Rs.2000 per day. (i.e 8lakhs above Rs.2000)

For this claim to be paid, the main claim must be admissible under section B1 of this policy. This benefit has a separate limit (over and above base sum insured) and does not affect cumulative bonus.

Limit for Daily Cash for Accompanying an Insured Child: Upto 0.25% of base sum insured and a maximum of ₹2000 per day. (over and above base sum insured).

B20. Second Opinion

We will provide You a second opinion from Network Provider or Medical Practitioner,if an Insured Person is diagnosed with the below mentioned Illnessesduring the Policy Period. The expert opinion would be directly sent to the Insured Person. (by sharing all the test report you can talk with a our doctors)

Cancer

Kidney Failure

Myocardial Infarction

Angina

Coronary bypass surgery

Stroke/Cerebral hemorrhage

Organ failure requiring transplant

Heart Valve replacement

Brain tumors

This benefit can be availed by an insured person once during a Policy Year.

B21. Maternity Cover (only delivery expenses – Must Use)

We will cover for Maternity Expenses, upto limits as specified in the table below, per policy subject to a waiting period of 4 years of continuous coverage under this policy .

Basic Sum Insured

Sub Limit

Up to Rs. 50 Lacs

A maximum of upto Rs 50,000/-. In case of birth of a girl child, the maximum limit under this coverage would be upto Rs 60,000/- per policy

Rs.75 Lacs to Rs.3 Crore

A maximum of upto Rs 1,00,000/-. In case of birth of a girl child, the maximum limit under this coverage would be upto Rs 1,20,000/- per policy

We will not cover ectopic pregnancy (fertilised egg implants itself outside of the womb, usually in one of the fallopian tubes) under this benefit (although it shall be covered under section B1).

Expenses incurred for following shall be excluded from the scope of this coverage:

Expenses incurred for pre/post natal care (during Pregnancy period)

Pre/Post hospitalization benefit (Section B2 and B3 of this policy)

In view of this coverage getting extended, maternity exclusion code 18 stands deleted. However, no coverage is available for voluntary termination of pregnancy during the policy period under this policy.

General Note:

No limit on No of deliveries..

No need that husband & Wife must be covered under same policy. this benefit is applicable for female Insured.

B22. Delivery Complications Cover

We will cover for medical expenses incurred for the medically necessary treatment of the new born baby upto limits as specified in the table below, for complications related to delivery if claim is admitted under the maternity benefit (B21) of this policy.

Basic Sum Insured

Sub Limit

Up to Rs.50 Lacs

Upto Rs. 10000

Rs. 75 Lacs to Rs. 3 Crore

Upto Rs. 25000

This benefit will trigger only in case where we have admitted the maternity claim

B23. First year Vaccinations (Mostly not opted)

We will pay for vaccination expenses for up to one year after the birth of the child subject to a limit (sub limit) of Rs. 10,000/- provided the child is covered with Us. In case of girl child, applicable limit under this coverage would be Rs.15,000/-.

For the claim to be paid under this benefit, the expenses related to maternity should be admissible under section B21 of this policy. The limit of Rs.10,000 (Rs.15,000 in case of girl child) is a lifetime limit and not a policy limit which will be applicable for each child.

This benefit will trigger only in case where we have admitted the maternity claim

B24. Prolonged Hospitalization Benefit

We will pay a fixed amount of 1% of sum insured,(sub limit) in the event of insured hospitalized for a disease/illness/injury for a continuous period exceeding 10 days.

This benefit will be triggered provided that the hospitalization claim is accepted under section B1 of this policy.

This benefit shall not be applicable for section B6 / B 31 of this policy.

This benefit has a separate limit (over and above base sum insured) and does not affect cumulative bonus.

Limit for Prolonged Hospitalization Benefit – 1% of Sum Insured (over and above base sum insured).

B25. High End Diagnostics

Feature Exclusive for Medicare Premier

We will cover for reasonable charges incurred for the following diagnostic tests only on OPD basis if required as part of a medically necessary treatment subject to limits as specified in the table below, per policy year:

Positron emission tomography Magnetic Resonance Imaging (PET MRI)

Renogram

Basic Sum Insured

Sub Limit

Up to Rs.50 Lacs

Up to Rs. 25,000 per policy year

Rs. 75 Lacs to Rs. 3 Crore

Up to Rs. 50,000 per policy year

This benefit has a separate limit (over and above base sum insured) and does not affect cumulative bonus.

B26. OPD Treatment (Must Use)

Feature Exclusive for Medicare Premier

Once the insured has completed two years of continuous coverage with Us, We will pay for expenses related to consultations and pharmacy up to limits specified in the table below, per policy year annually subject to policy terms and conditions.

Basic Sum Insured

Sub Limit

Up to Rs.50 Lacs

Upto Rs. 5,000/-

Rs.75 Lacs

Upto Rs. 7,500/-

Rs. 1 Crore

Upto Rs. 10,000/-

Rs. 2 Crore

Upto Rs. 15,000/-

Rs. 3 Crore

Upto Rs. 20,000/-

This benefit has a separate limit (over and above base sum insured) and does not affect cumulative bonus.

B27. OPD Treatment – Dental

Once the Insured has completed two years of continuous coverage with Us, we will pay for expenses related to the following dental treatments only subject to a maximum of limit specified in the table below, per policy year annually:Only 3

Root Canal Treatment (single or multiple sittings)

Tooth extraction(s)

Filling

Basic Sum Insured

Sub Limit

Up to Rs. 50 Lacs

Upto Rs. 10,000/-

Rs. 75 Lacs

Upto Rs. 12,500/-

Rs.1 Crore

Upto Rs. 15,000/-

Rs.2 Crore

Upto Rs. 20,000/-

Rs.3 Crore.

Upto Rs. 25,000/-

This benefit has a separate limit (over and above base sum insured) and does not affect Cumulative Bonus.

In view of this coverage getting extended, dental exclusion (General Exclusions ii. 1. ix) is not applicable for this particular coverage.

B28. Emergency Air Ambulance Cover

We will pay for ambulance transportation of the Insured Person in an airplane or helicopter subject to maximum of limit specified in the table below, for emergency life threatening health conditions which require immediate and rapid ambulance transportation to the hospital/medical centre for further medical management.

The Medical Evacuation should be prescribed by a Medical Practitioner and should be Medically Necessary.

This benefit shall only be payable if We have accepted an inpatient Hospitalization claim for the Insured member under section B1 of this policy.

Basic Sum Insured

Sub Limit

Up to Rs.50 Lacs

Up to Rs. 500,000

Rs.75 Lacs to Rs. 3 Crore

Up to Rs. 500,000 for Non Network; Upto Sum Insured for Network Provider

This benefit has a separate limit (over and above base sum insured) and does not affect Cumulative Bonus.

B29. Accidental Death Benefit

If an Insured Person suffers an accident during the policy period and this is the sole and direct cause of his death within 365 days from the date of accident, then We will pay a fixed amount of 100% of the base Sum Insured,maximum up to Rs 50 Lacs(Sub Limit).

Note: it is fixed amount for each died person.

This benefit is not applicable for dependent children covered in the policy.

limit for Accidental Death Benefit: 100% of base Sum Insured, maximum Upto Rs.50 Lacs (over and above base sum insured)

B30. Cumulative Bonus/ No Claim Discount

50% cumulative bonus will be applied on the Sum Insured for next policy year under the Policy after every claim free Policy Year, provided that the Policy is renewed with Us and without a break. The maximum cumulative bonus shall not exceed 100% of the Sum Insured in any Policy Year.

If a Cumulative Bonus has been applied and a claim is made, then in the subsequent Policy Year We will automatically decrease the Cumulative Bonus by 50% of the Sum Insured in that following Policy Year. There will be no impact on the Inpatient Sum Insured, only the accrued Cumulative Bonus will be decreased.

In policies with a tenure of more than one year, the above guidelines of Cumulative Bonus shall be applicable post completion of each policy year

In relation to a Family Floater, the Cumulative Bonus so applied will only be available in respect of those Insured Persons who were Insured Persons in the claim free Policy Year and continue to be Insured Persons in the subsequent Policy Year.

For purpose of computation of Cumulative Bonus, the percentage (%) of Cumulative Bonus will be applied on the base Sum Insured only. Restored sum insured will not be taken into consideration.

Cumulative Bonus shall be provided only if No Claim Discount has not been availed for the claim free previous Policy Year.

If you Choose No Claim Discount, We will allow 1% discount on renewal premium for every claim free Policy Year, provided that the Policy is renewed with Us without break.

B31. Home Care Treatment Cover (Applicable only for Sum Insured Rs.75 Lacs and above)

We will cover for reasonable and customary medical expenses incurred for treatment taken at home, which are “Equivalent Medical charges” as defined in this policy, for below specified conditions/illness upto the sum insured (excluding accrued cumulative bonus) for the Insured Person’s medically necessary treatment at home. Restore benefit sum insured is not applicable for this benefit.

Basic Sum Insured (Rs.)

sub Limit

Up to Rs. 50 Lacs

NA

Rs. 75 Lacs to Rs. 3 Crore

Upto Sum Insured for 1. Dialysis at home 2. Cancer care (Chemotherapy) at home 3. Up to 25% of base sum insured excluding cumulative bonus for Pandemic Care at home, max up to 15 days in a policy year

Home Care Treatment means treatment availed by the Insured Person at home for below listed conditions/ illness/ procedures, which in normal course would require hospitalization of more than 24 hours or would have been admissible under Day Care Procedures but is actually taken at home provided that:

The medical practitioner advices the insured person to undergo treatment at home.

There is a continuous active line of treatment with monitoring of the health status by a medical practitioner for each day through the duration of the home care treatment.

Daily monitoring chart including records of treatment administered duly signed by the treating doctor is maintained

Home care treatment is availed in India.

Home treatment services may be provided through network service provider/ empanelled service provider in select cities for select treatment procedures only. Please contact us or visit our website (www.tataaig.com) for updated list of treatment procedures and cities where home treatment service is provided.

Insured shall be permitted to avail the services as prescribed by the medical practitioner.

In case the insured intends to avail the services of non-network provider, claim shall be subject to reimbursement, a prior approval from the insurer needs to be taken before availing such services from a registered home care provider. Insurer shall respond to approval request within 4 working hours of receiving the last necessary requirement.

Specified conditions/ illness covered under Home care treatment:

Dialysis at home (for kidney patient)

Chemotherapy at home(for cancer)

Pandemic Care at home(COVID-19) for a maximum period of 15 days and maximum upto 25% of the base sum insured excluding cumulative bonus (Pandemic as defined and declared by World Health Organization (WHO) or any equivalent healthcare authority)

In this benefit, the following shall be covered if prescribed by the treating medical practitioner and is related to treatment covered under the policy,

Diagnostic tests undergone at home or at diagnostics center

Medicines prescribed in writing

Consultation charges of the medical practitioner

Nursing charges related to medical staff

Medical procedures limited to parenteral administration of medicines.

Including but not limited to cost of Pulse Oximeter, Oxygen cylinder and nebulizer wherever applicable

For the purpose of this cover,“Equivalent Medical charges” shall mean the charges for services or supplies, which are the standard/equivalent charges for the specific provider and not more than the prevailing charges in the geographical area for identical or similar services taken on inpatient/day care basis, considering the nature of the illness / injury involved.

B32. Wellness Services (practically not applicable but Must use)

We / our Empanelled Service Provider will provide below mentioned wellness services designed to assist insured persons in maintaining and improving good health and fitness. These Wellness Services will be available for the insured person during the policy period and as specified in the Policy schedule.

1.Teleconsultation – General

We /our empanelled Service Provider will arrange for teleconsultations upon insured person’s request through telecommunications and digital communication technologies for insured person’s health related complaints or preventive health care by a qualified Medical Practitioner/ Health Care Professional, as per the limit specified in your Policy Schedule.

This service can only be availed subject to condition below:

– Consultation will be provided through various specified modes of communication (including but not limited to) like audio, video, online portal, chat, digital customer application or any other digital mode.

2. Teleconsultation – Speciality

We /Our empanelled Service Provider will arrange for teleconsultations upon insured person’s request through telecommunications and digital communication technologies for insured person’s health related complaints or preventive health care by a qualified & specialist Medical Practitioner/ Health Care Professional, as per the limit/speciality specified in your Policy Schedule.

This service can only be availed subject to conditions below:

– Consultation will be provided through various specified modes of communication (including but not limited to) like audio, video, online portal, chat, digital customer application or any other digital mode.

3. Ambulance Booking facility

We / Our empanelled Service Provider will provide a facility to book a road ambulance in India, for transportation of an Insured Person to a Hospital for admission or from one hospital to another hospital for better medical facilities and treatment.

This booking service can be availed at Our Network subject to the transportation of the Insured Person will be offered to the nearest Hospital

4. Emergency – Help me feature

In case of an emergency, insured person will have an option to share his/her location with the ‘designated caregiver’ through our customer application provided the insured person has registered on our App.

The app will trigger a message and call to the designated caregiver informing about the emergency and sharing the location of the Insured Person.

For the purpose of this benefit, ‘designated caregiver’ shall mean that individual who has been specified as a caregiver at the time of registration in the customer App.

Please note

– This service will be available subject to suitable infrastructure, connectivity, device restrictions and device functionality.

5. Redeemable voucher/Discount on services

We / our empanelled service provider will provide redeemable vouchers/ discount (as approved by the regulator from time to time) on certain specified products/ services to promote wellness and fitness, Discounts on Pharmacy & Diagnostics of the insured person.

6. Health Condition Management

We / our empanelled service provider will provide consultative services related to health conditions/ illnesses with the objective of maintaining good health and improving it through various health condition management programmes including but not limited to nutrition management, weight management, chronic condition management, stress management, health coach (as approved by the regulator from time to time) and offered by us.

Consultative services will be provided through various specified modes of communication (including but not limited to) audio, video, online portal, chat, digital customer application or any other digital mode.

Definition:

For the purpose of section B 32 of this policy, a Health Care Professional is a person who holds a valid qualification from regulatory body as set up by the Government of India or a State Government or any other relevant authority and is engaged in actions with an objective of maintaining and improving individual’s good health.

B33. Wellness Program (practically not applicable but must use)

We / our empanelled service provider will provide a wellness program designed to promote wellness and fitness amongst the insured persons. This wellness program is structured to reward the insured person in the form of measurable wellness score for the prescribed physical efforts/fitness activity undertaken by such insured person during the policy period. This is a voluntary program available for insured with age above 18 years, at the start of the policy year. It is advisable to the insured person to consult his/her physician before starting any physical exercise/ activity.

It is a pre-condition for enrolment under this wellness programme, that the insured person should have undergone the health risk assessment as specified below and depending on the outcome from health risk assessment, the wellness reward and its scoring should be administered. The earnings under the wellness program is linked to your wellness category and shall be valid for one year from the date of credit of daily score in insured person’s wellness account, provided the policy is renewed within the grace period. Daily score will be credited after the completion of a healthy day.

For the purpose of understanding if the daily score is credited on 1st Jan 2024 it will be valid up to 31st Dec 2024.

Health risk assessment

We / our empanelled service provider will provide a health risk assessment (HRA) questionnaire, which is an online tool for evaluation of status of health and quality of the insured person’s life. This tool helps insured persons to review their lifestyle practises which may impact their health status.

To undertake the health risk assessment, you can log into your account on our customer application. This can be undertaken once a policy year.

On completion of the health risk assessment and based on the insured person’s assessment results, we / our empanelled service provider will identify the wellness category in which the insured person falls in.

Wellness categories for this purpose are defined as below:

Green – low risk for developing lifestyle disease as compared to peers in the same age and gender group.

Yellow – moderate risk for developing lifestyle disease as compared to peers in the same age and gender group.

Red – higher risk for developing lifestyle disease as compared to peers in the same age and gender group.

The overall wellness category is valid till the expiry of the policy year in which the insured undergoes the assessment and will be updated based on HRA results of subsequent assessment undergone by the insured person in each consecutive policy year, subject to renewal of the policy within the grace period. In the event of a long- term policy (greater than 1 year) the insured has to undergo HRA in each policy year to be eligible for wellness rewards. If the insured does not undergo assessment in the consecutive policy year, henceforth no rewards will be earned for any physical activity undertaken. However, earned rewards will be carried forward till its validity and will be available for utilization.

2. Wellness Rewards

Mechanism to earn Wellness Reward:

We will encourage physical exercise and fitness and recognise the effort by rewarding the insured person on daily basis for each healthy day.

A healthy day can be earned by undertaking below activity on a calendar day:

Recording 10, 000 steps / day# in the activity tracking apps or fitness tracker devices as prescribed by the company or our empanelled service provider: or

Burning 500 calories or more in a day through activity as measured by fitness tracker devices.

The company may at its discretion change the above criteria and the same would be mentioned in the policy schedule/ customer application.

Wellness reward will be earned depending on the wellness category of the insured person and as per the grid below:

Wellness category

Green

Yellow

Red

Rewards per Healthy Day

10

7

5

Note:

HRA registration will be allowed anytime during the policy year and healthy activities will be tracked throughout the policy year, however, for each policy year, activities completed in first 300 days of the policy year will be considered for reward in the same year, activities completed on or after 301st day of the policy year will be carried forward to the next policy year and will be available for utilization in the next year provided the policy has been inforce or renewed with us without any break within the grace period.

In case of individual policy, each insured person would be tracked separately and shall earn wellness reward based on one’s own individual performance/physical activity as per the grid above

In case of family floater policy,each insured person, with age above 18 years, at the start of the policy year, would be tracked separately and shall earn wellness reward based on one’s own individual performance/physical activity as per the grid above. In order to compute the wellness reward for such policies, average of individual performance rewards would be considered for computation of wellness reward.

# The company may also use alternative measurement criteria in lieu of steps and calories burnt and the same shall be mentioned on the policy schedule

Data entered manually in the fitness tracking apps or devices will not be considered for tracking healthy day

Calories burnt during basic metabolism shall not be considered for tracking healthy day (here basic metabolism refers to activities done while at rest to maintain vital functions such as breathing and keeping warm etc.)

Mechanism to Utilise Wellness Reward:

Wellness Reward accumulated through fitness activities can be converted into monetary value as per method defined below and can be utilized towards the payment of services/items under below categories, available through our Network/ empanelled service provider:

OPD consultation/ treatment

Pharmaceuticals

Health-check-ups/ diagnostics

Health Supplements

Coverage of cost of treatment of any admissible claim in respect of non-payable items that are specified under the terms and conditions of the base policy Or any other items as prescribed by the company or our empanelled service provider as approved by the Regulator as a redeemable item from time to time.

Note:

Wellness Reward can be converted into a monetary value after every Healthy Day, during the Cover Period

Monetary value of the Wellness score earned is equivalent to the:

Wellness score earned X (Per year Policy Premium without Taxes/ 10,000).

In case of policy with tenure more than one year, ‘per year policy Premium without Taxes’ = (Total Policy premium without tax, for the tenure/ policy tenure).

In case of family floater policy, reward will be calculated on average premium per person which is equivalent to the Total Policy premium without tax/ number of Insured persons covered in the policy on floater basis

Illustration

Age of the Insured Person (Years)

40

Sum Insured opted under the Policy (Rs.)

5 Lacs

Plan Type

Individual

Policy Tenure (years)

1

Total number of members covered under the policy

1

Net Premium paid (without Tax)

7931

Wellness Category (post Health Risk Assessment)

Green

Healthy Day

Wellness Reward earned (per day)

Wellness Reward converted to Monetary Value (per day)

Wellness Reward credited after Healthy Day

Wellness Reward valid up to 365 days (provided the policy is active and insured is covered)

1 to 300 day

10

7.931

Date of credit of Wellness score

365 days from the Date of credit of Wellness score

301 day onwards

10

7.931

Date of Policy Anniversary – in case of Multi year policy Date of renewal – in case of 1 yr policy

365 days from: Date of Policy Anniversary – in case of Multi year policy – Date of renewal – in case of 1 yr policy, as applicable

Maximum Total in a Policy Year

2894.82

Steps to register for Wellness Program and earn & spend Wellness Rewards

Step 1. Register yourself on customer application

The insured person will download Tata AIG customer application on your device and complete registration process by providing policy and insured person’s details.

Step 2. Complete health risk assessment

Submit response to the online health questionnaire on your device.

On completion of the health risk assessment, a Wellness category will be assigned to the insured person for the policy year and will be updated based on the latest health risk assessment in next policy year.

Step 3. Comply with mechanism to earn Wellness Rewards

We will track the physical exercise and fitness activities completed by the insured person, through the customer app.

Activities completed on a calendar day will be considered as a Healthy Day and reward will be credited to insured person’s wellness account.

Step 4. Convert Healthy Day into monetary value and spend

Insured person will have an option to convert the accumulated rewards into the monetary value and spend it on items/ services offered under the policy

The unutilized rewards will be carried forward to next Policy year till this policy is renewed with us within grace period and is inforce subject to validity period of the reward point)

Disclaimer (applicable to section B32 & B33)

Availing the services under this benefit is purely upon the Insured’s sole discretion and risk.

For services that are provided through empanelled Service Providers, we are acting as a facilitator; hence would not be liable for any incremental costs or the services. Any additional services availed, or expenses incurred on such services or benefits which are other than those covered under this policy and explicitly excluded by this policy schedule, shall not be covered under this policy and all expenses incurred shall be borne by the insured person.

We shall not be responsible for or liable for, any actions, claims, demands, losses, damages, costs, charges and expenses which insured person claims to have suffered, sustained or incurred, by way of and / or on account of the benefit. We shall not be liable for any deficiency or discrepancy in the services provided by empanelled service provider/network provider under this policy.

Insured person may consult any medical professional at any network provider/empanelled service provider at its sole discretion. The cost of service arising out of insured person choice of medical professional at any network provider/emplaned service provider shall be completely borne by the insured person unless covered otherwise. However, the services under this policy should not be construed to constitute medical advice and/or substitute the insured person’s visit/ consultation to an independent medical practitioner/healthcare professional

The medical practitioner may suggest/recommend/prescribe over the counter medications based on the information provided, if required on a case-to-case basis. Provided that any recommendation under this policy shall not be valid for any medico legal purposes.

The insured person is free to choose whether or not to act on the recommendation after seeking consultation.

Any advice, recommendations or suggestions made by any medical professional shall be solely based on the information and documentation provided by the insured person to such medical professional. We shall not be liable towards any loss or damage (immediate or consequential) arising out of or in relation to any opinion, advice, prescription, actual or alleged errors, omissions and representations made by the medical professional from whom we have availed services or taken benefit or for any consequence of any act or omission in reliance thereon.

We at our discretion may provide discounts on any of the above services

Any discount offered under redeemable voucher/discount on services by our empanelled service providers are subject to modification or withdrawal. We do not assume any liability towards the quantum of discount, quality of product/services and timeline within which the product/service is rendered.

For Ambulance Booking facility–

These services are provided through our empanelled service provider in select cities. Please contact us / refer to our digital customer application for more details on this service.

We do not assume any liability towards quality and turnaround times of service rendered, any loss or damage arising out of or in relation to these services rendered by the empanelled service provider.

This facility may be availed through Our digital customer application or through calling Our call centre on the tollfree number specified in the Policy Schedule.

Above mentioned services are non-portable, annual contracts, independent of policy contract and not lifelong renewable. The Services provided may be added / deleted / modified at our discretion and the same shall be notified to the policyholders in advance prior to change effective date.

Provision of these services is subject to availability as per the duration specified by Us/the empanelled service provider. Details are available on our website (www.tataaig.com)

Any service availed by the Insured Person under this Benefit will not impact Cumulative Bonus if applicable.

We reserve the right to change any service provider during the currency of the policy or at renewal. The same shall be intimated to the insured atleast 15 days prior to the effective date of change. During such change, all the credits earned by the insured person shall be transferred to the new service provider.

In case we or the assistance service provider fails to provide any of the services as mentioned in this policy or is unable to implement, in whole or in part due to force majeure, non-availability of services, change in law, rule or regulations which affects the services, or if any regulatory or governmental agency having jurisdiction over a party takes a position which affects the services , then the assistance services’ suspended, curtailed or limited performance shall not constitute breach of contract and the company or the assistance service provider shall have no liability whatsoever including but not limited to any loss or damage resulting therefrom.

Tax Benefit:

The premium amount paid under this policy qualifies for deduction under Section 80D of the Income Tax Act.

Section 3 –Exclusions (Must Read)

General Note:CODE related exclusion are same for all insurance companies (IRDAI rule). remaining exclusion also same but with different terminology.

General Exclusions

We will neither be liable nor make any payment for any claim in respect of any Insured Person which is caused by, arising from or in any way attributable to any of the following exclusions, unless expressly stated to the contrary in this Policy.

1. Standard Exclusions

A. Exclusions with waiting periods (5 kinds of waiting periods)

1. 30 Days Waiting Period (Code-Excl03):

Expenses related to the treatment of any illness within 30 days from the first policy commencement date shall be excluded except claims arising due to an accident, provided the same are covered.

This exclusion shall not, however, apply if the Insured Person has Continuous Coverage for more than twelve months.

The within referred waiting period is made applicable to the enhanced sum insured in the event of granting higher sum insured subsequently.

2. Specified Disease/Procedure Waiting Period (Code-Excl02):excluded until the expiry of 24 months

Expenses related to the treatment of the listed Conditions, surgeries/treatments (40) shall be excluded until the expiry of 24 months of continuous coverage after the date of inception of the first policy with us. This exclusion shall not be applicable for claims arising due to an accident.

In case of enhancement of sum insured the exclusion shall apply afresh to the extent of sum insured increase.

If any of the specified disease/procedure falls under the waiting period specified for pre-Existing diseases, then the longer of the two waiting periods shall apply.

The waiting period for listed conditions shall apply even if contracted after the policy or declared and accepted without a specific exclusion.